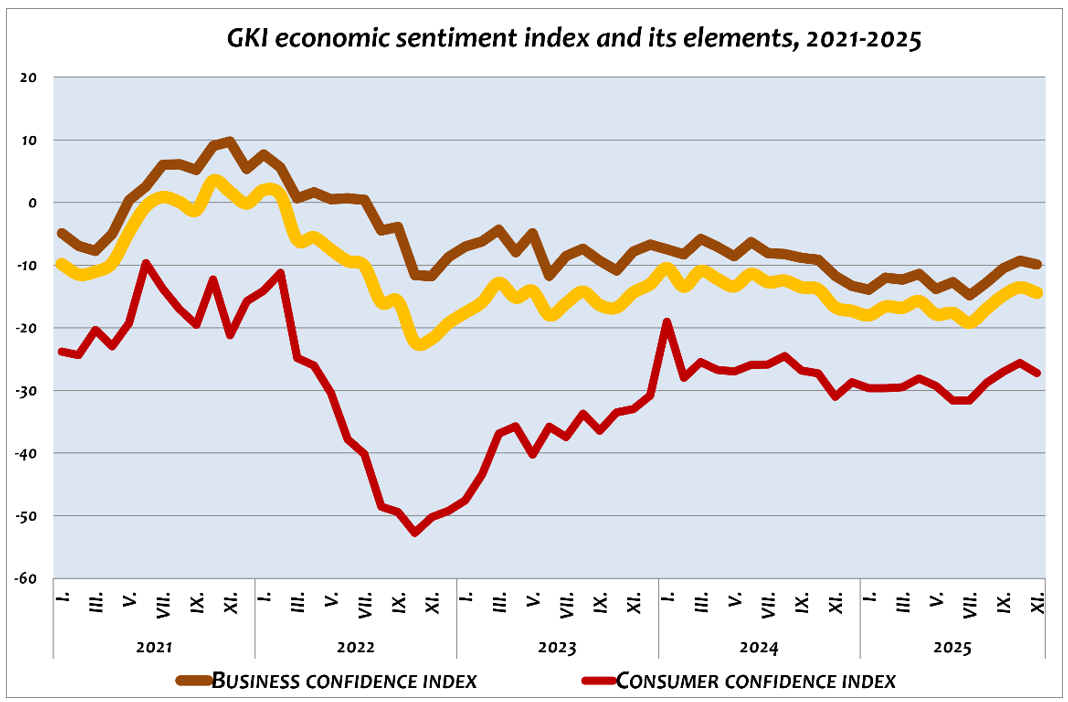

According to the survey conducted by GKI Economic Research Co., supported by the EU, business expectations changed little in November, while consumers adopted somewhat more downbeat views than in October. The composite indicator summarising these expectations – the GKI economic sentiment index – fell by just under one point, a shift within the margin of error. Firms’ willingness to hire continued to improve, yet aggregate expectations regarding future sales prices rose compared with the previous month. Respondent companies reported no change in the predictability of the business environment during the final month of autumn.

The GKI business confidence index – after three months of gains – slipped in November compared with October, though only within the margin of error. The slight retreat was driven solely by industry, whose confidence indicator fell by two points. The construction index was unchanged, while the retail and services indicators each rose by two points. The retail indicator has not stood this high for fourteen months, nor the services indicator for thirteen. Looking ahead, construction remains the least, and business services the most, optimistic sector.

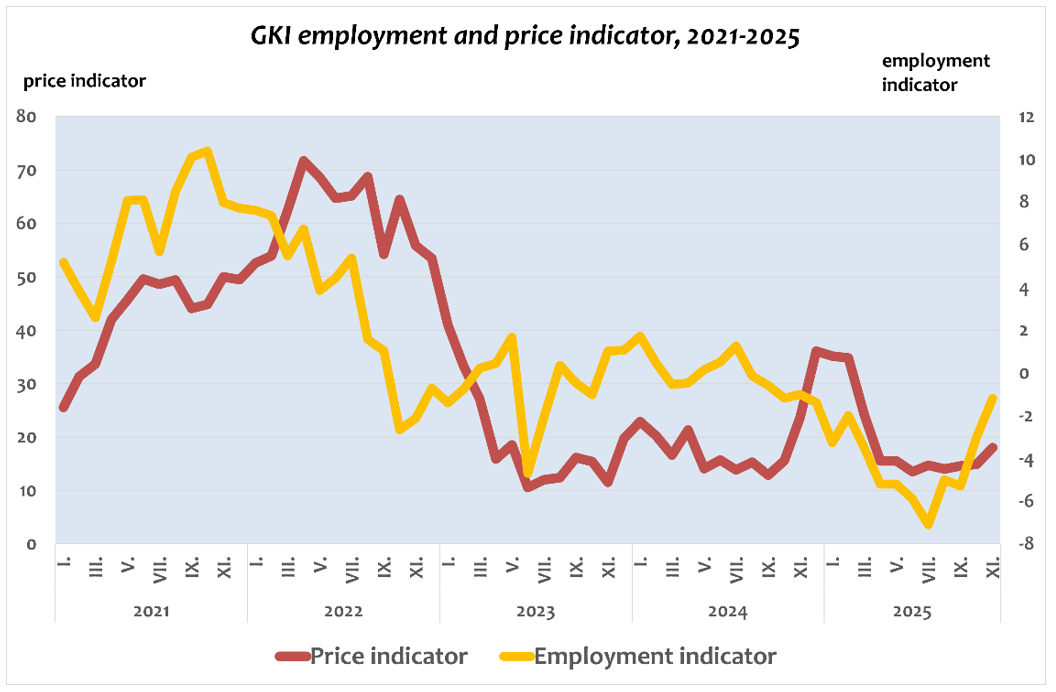

The employment indicator, which reflects firms’ overall staffing intentions, rose markedly compared with the previous survey, reaching its highest level in a year. Over the next three months, 8% of companies plan to expand their workforce, while 12% expect to reduce it.

The predictability of the business environment showed no meaningful change in November compared with the previous survey. Industrial and construction firms remain the most troubled by the lack of predictability, whereas retail and service companies are less affected.

The price indicator, which tracks firms’ expected sales prices over the coming three months, rose slightly in November compared with the previous survey, following three months of stagnation. Over the next quarter, 26% of companies intend to raise prices, while 8% plan to cut them. A month earlier, the corresponding figures were 19% and 8%.

The GKI consumer confidence index reached a fourteen-month high in October. November, however, brought a negative correction: the index fell by nearly two points on a monthly basis. Households’ assessment of their financial situation over the past twelve months deteriorated noticeably, and their financial outlook for the coming year worsened slightly compared with October. Expectations regarding the country’s economic prospects over the next twelve months improved a little further. Views on the amount of money available for major household purchases were unchanged. Inflation expectations showed no shift, while prospects for the future number of unemployed improved markedly.

Data for the charts can be found in the attached Excel file.

Methodological Explanation:

GKI Economic Research Co., following the methodology prescribed by the European Commission, calculates its economic sentiment index by integrating expectations from both the business sector and households (consumers). Specifically, the GKI economic sentiment index is a weighted average of the consumer confidence index and the business confidence index.

The GKI business confidence index itself is a weighted average of confidence indicators from four sectors: industry, retail trade, construction, and services. The employment indicator reflects the net balance of firms planning to increase or decrease their workforce over the next three months. Similarly, the price indicator measures the net difference between companies intending to raise or lower their selling prices within the same period.

The GKI consumer confidence index is computed as the arithmetic mean of balance indicators derived from survey responses regarding households’ assessments of their financial situation over the past twelve months, their financial outlook for the next twelve months, expectations for the country’s economic performance, and intentions to purchase durable goods.

GKI publishes seasonally adjusted data, employing appropriate mathematical techniques to eliminate distortions caused by seasonal factors – such as heightened demand before Christmas or reduced production during summer holidays.

Download full study