The stock of household credit in Hungary rose dynamically between 2017 and the first quarter of 2025, with the value of household loans expanding by roughly 118%. Within this, between the second quarter of 2024 and the second quarter of 2025 the stock grew by 11.7% – the fifth-highest rate among the EU’s 27 member states. For comparison, the figure was 7.1% in the Czech Republic, 5.6% in Slovakia and 3.6% in Poland. The further strengthening of domestic credit dynamics has also been supported by the Otthon Start housing-loan scheme. Rapid credit expansion, however, increases repayment obligations and, through this channel, exerts a dampening effect on consumption.

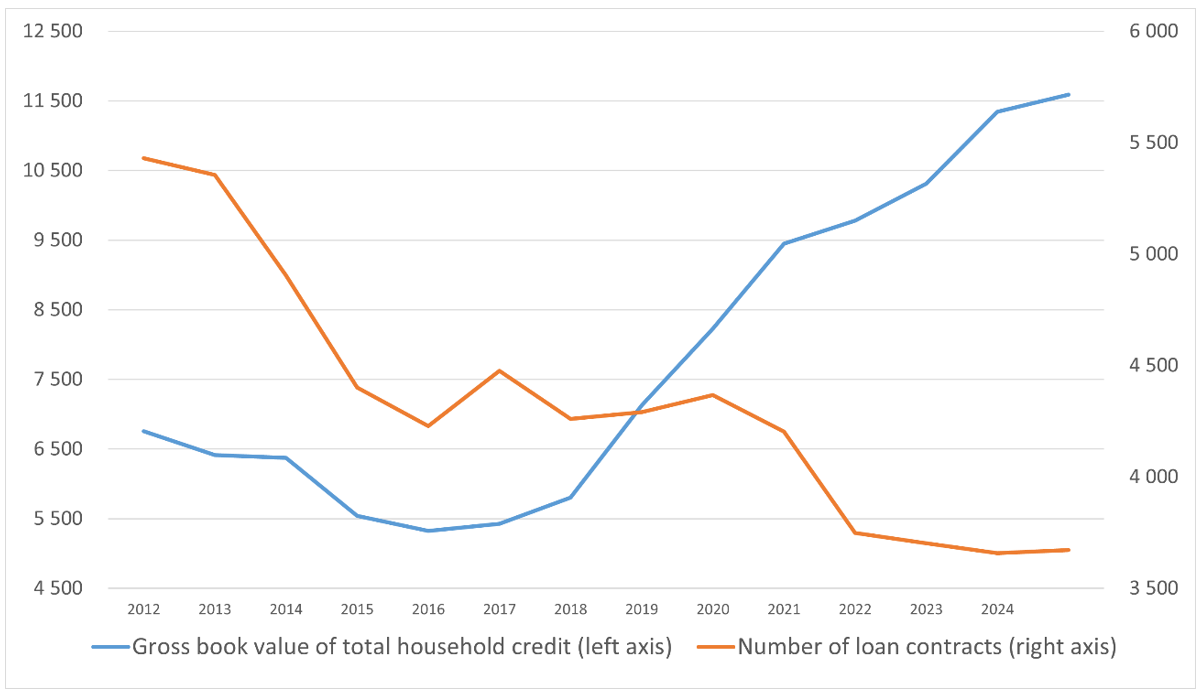

Since 2016 the household credit stock has expanded year after year, even as the number of loan contracts has steadily declined. Between 2012 and the second quarter of 2025 the number of loan contracts fell by 32.4%, while the stock rose by 71.5%. This implies that the average value of outstanding loans – and thus the size of monthly repayments – has increased. One of the key drivers of credit growth has been rising household incomes and surging property prices. Between 2017 and 2024 both employee incomes (+104%) and the household credit stock (+109%) roughly doubled.

Rising loan repayments reduce households’ disposable income, thereby restraining consumption. This matters in several respects: consumption is, on the one hand, a key indicator of living standards; on the other, household spending forms the basis for a substantial share of government revenues (such as VAT receipts).

The Evolution of the Number of Loan Contracts (thousands) and the Stock of Household Credit (billion forints)

Source: MNB

In 2014 total annual household loan repayments amounted to 1,668 billion forints, while by 2024 they had reached 3,075 billion. This corresponds to an 84% nominal increase over ten years – an average annual nominal growth rate of 6.3%. In real terms, this represents an expansion of 11.6%.

In 2024, household spending on principal and interest repayments accounted for 7.6% of total private consumption. This ratio was 15.3% in 2012 and has followed a declining trend since, reflecting the expansion of household consumption. At first glance, this appears to be a positive development. Yet many social groups typically do not take out – or cannot access – credit, giving the picture a more nuanced character. The figures also exclude loans that have left the banking system and been transferred to debt-collection agencies.

In September 2025 GKI conducted a nationwide, representative survey of 1,000 people to examine household repayment burdens and their impact on consumption. Some 38.5% of households hold some form of debt. Broken down by age, indebtedness is highest among those in their thirties, 55.8% of whom have a loan. The share of borrowers is particularly high among households with unemployed members, which poses significant long-term social risks: while 45% of active earners have a loan, the figure rises to 50% for households with unemployed members. Admittedly, for the latter group, loan repayments account for “only” 21% of income. Bankmonitor notes that after a long period of decline, the number of individuals on the KHR (formerly BAR) list began rising again in March 2025.

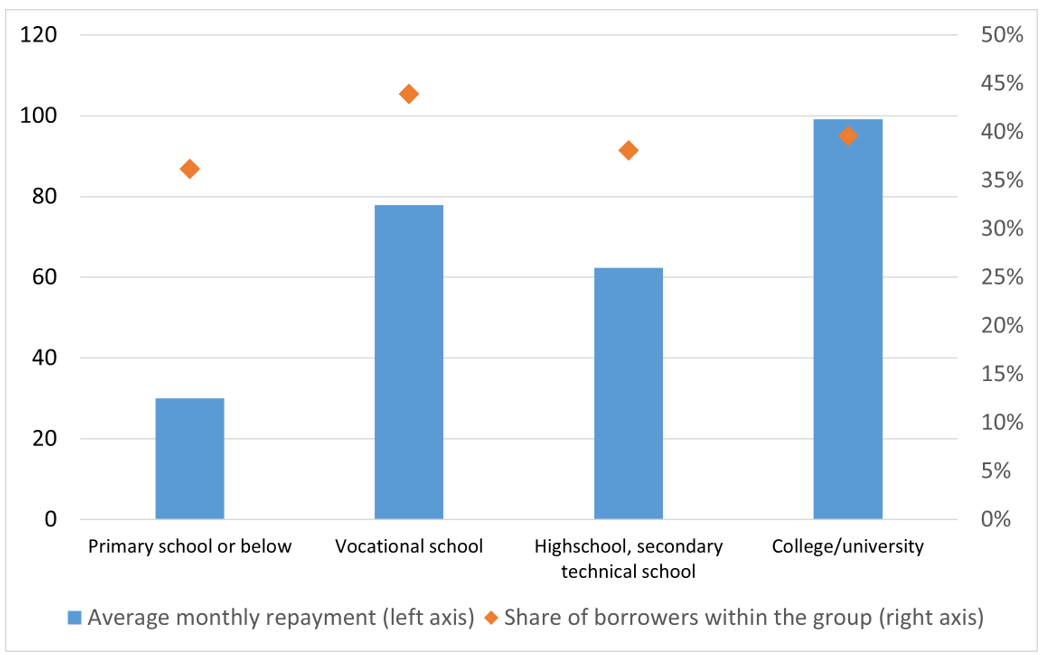

Share of Borrowers (%) and Average Monthly Repayment (thousand forints) by Education Level

Source: GKI Survey

By education level, the highest share of borrowers is found among skilled workers (43.9%). Yet the largest average monthly repayments are typical of those with higher education: around 98,000 forints, consuming roughly 23% of their net income.

From a consumption standpoint, the crucial measure is the ratio of repayments to income, as it indicates the extent to which debt burdens reduce households’ disposable income. While average monthly repayments vary considerably by education, income level, and occupation, the share of repayments relative to family income differs less across social groups. On average, households allocate 15.4% of their income to loan repayments, and although this share declines with rising income, it still exceeds 10% even among the highest earners.

Overall, Hungary’s household credit market in recent years has exhibited both rapid growth in the stock of loans and a narrowing pool of borrowers. Repayments significantly reduce households’ disposable income, thereby restraining consumption and indirectly affecting government revenues. The Otthon Start programme continues to encourage credit expansion, potentially reinforcing these existing trends. This underscores the importance of taking the evolution of household debt into account when analysing consumption and savings patterns.