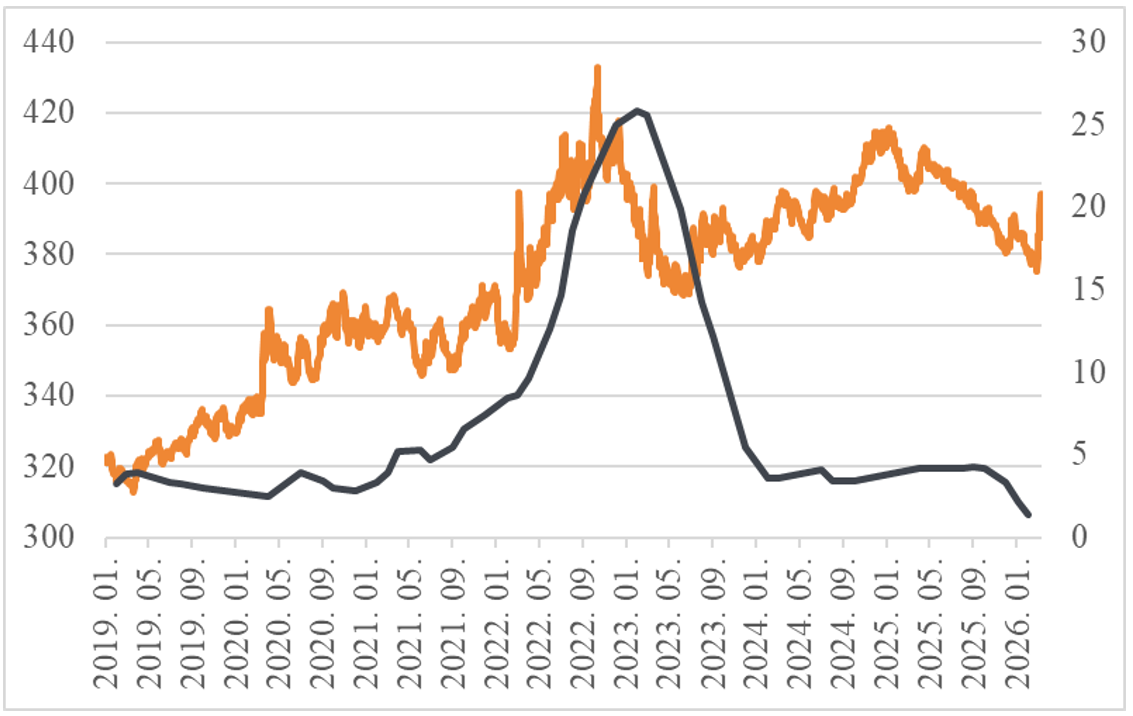

According to the latest data from Hungarian Central Statistical Office, consumer prices in February 2026 were only 1.4% higher than a year earlier, pointing to a notably subdued inflationary environment. The modest price index—falling short of analysts’ expectations—can be attributed to several factors. Most importantly, the prices of several food products have declined markedly over the past year, including margarine, flour and some dairy products, exerting downward pressure on the headline figure, partly as a result of margin caps and partly due to increased import substitution. At the same time, motor-fuel prices fell by more than 11% year on year, adding a further substantial disinflationary impulse.

The euro–forint exchange rate (orange, left axis) and the monthly consumer price index (black, right axis), January 2019–March 2026

Source: MNB, KSH

The structure of inflation, however, remains uneven. Service prices rose by 4.2%, suggesting that domestic price pressures—driven largely by wage dynamics and demand-side factors—remain present in the economy. Rising wages naturally feed through into the price of services, where labour costs typically account for a large share of total expenditures.

Following the favourable January inflation reading, the Magyar Nemzeti Bank cut its base rate to 6.25%. February’s low inflation data would, in principle, support further easing. Yet the recent outbreak of conflict in the Middle East clouds the outlook for consumer prices through two distinct channels. First, a surge in energy prices is likely to feed through into the cost of both goods and services. Second, an exchange rate that may remain elevated would raise import costs. Heightened uncertainty compounds the problem, manifesting itself in increased volatility in the domestic currency. As a small, open economy with a substantial dependence on energy imports, Hungary is particularly exposed to these external shocks. In such an environment it remains uncertain whether the central bank will proceed with another rate cut in March.

The current low inflation rate partly reflects the relatively strong exchange rate observed in recent months as well as favourable base effects. Should the forint remain persistently volatile—or should global energy prices stay elevated—renewed inflationary pressures may re-emerge in the Hungarian economy in the coming period, which could potentially delay the improvement in the interest rate environment.