Based on the state of the current year’s budget as of April (with 71% of the annual deficit already reached within the first four months), it is evident that this year’s fiscal targets are no longer sustainable. This recognition is underscored by the Ministry for National Economy’s recent upward revision of the 2024 deficit to 4.1% of GDP. Since the projected budget revenues and their long-term effects were not updated in the 2026 draft budget, it is almost certain that the fiscal figures for 2026 will not materialize as outlined in the proposal.

A particularly problematic aspect of next year’s budget is the phased revenue loss stemming from the lifetime personal income tax (PIT) exemption granted to mothers of two and three children. This exemption will progressively reduce budget revenues over the coming years. The following analysis by the GKI Economic Research Co. outlines the expected impacts through 2029:

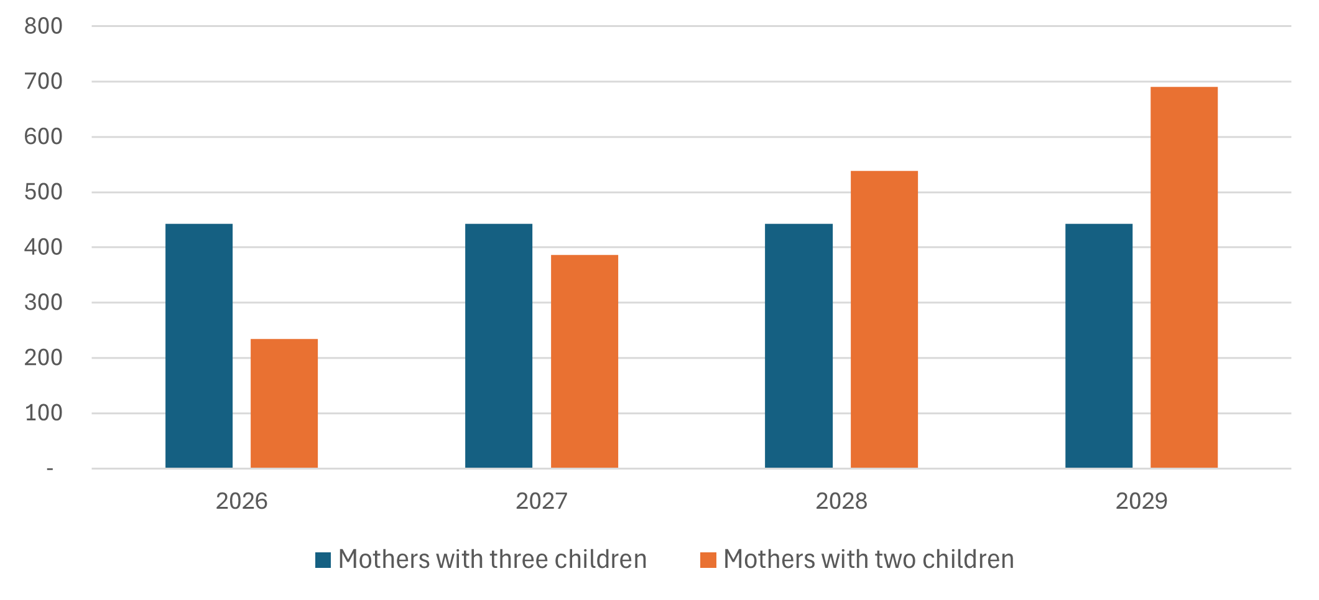

The government is introducing the PIT exemption for mothers with two children in four age-based cohorts. Assuming an even distribution of the approximately 600,000 eligible mothers (as cited by the Minister for National Economy), the estimate assumes 150,000 new beneficiaries per year. Based on current income quintiles and assuming a nominal wage growth of 12% by 2026, the total cost of the exemption for mothers with two children is projected to reach HUF 190 billion in 2026[1]. However, a portion of the resulting increase in net incomes will be spent[2], generating approximately HUF 25 billion in VAT revenue for the state. This mitigates the net revenue shortfall to HUF 165 billion.

In addition to the PIT exemption, the government is doubling the family tax credit for two-child households—from HUF 20,000 to HUF 40,000 per child. With 340,000 households affected, this will result in a further HUF 80 billion in lost revenue, bringing the total fiscal impact for this group to HUF 245 billion in 2026.

By 2029, when the PIT exemption applies universally to all mothers with two children regardless of age, the annual revenue loss is projected to reach HUF 770 billion based on 2024 earnings. Assuming a 30% nominal wage increase by 2029, the gross revenue impact could rise to HUF 1,000 billion. Accounting for increased consumer spending and the associated tax revenues, the net budgetary impact is estimated to be approximately HUF 700 billion.

For mothers with three children, eligibility for the PIT exemption begins universally on October 1, 2024. For comparative purposes, the estimated budgetary impact is calculated for the full year 2026. With 250,000 eligible women, the cost in foregone PIT revenues is expected to be HUF 290 billion. Increased consumption could yield HUF 30 billion in additional VAT revenue. Moreover, the doubling of the family tax credit (from HUF 100,000 to HUF 200,000 per month) for three-child households—affecting approximately 130,000 households—adds another HUF 150 billion to the fiscal cost.

Altogether, the support provided to three-child mothers will amount to HUF 410 billion in 2026. When combined with the fiscal costs of benefits for two-child mothers, the total package is expected to reach HUF 655 billion next year.

Net Budgetary Impact of PIT Exemption and Doubled Family Tax Credits for Mothers of Two and Three Children, Adjusted for Increased Consumption (HUF billion, 2025–2029) Source: GKI calculations, based on 2024 income data.

Source: GKI calculations, based on 2024 income data.

In addition to unresolved practical and social questions—such as whether eligibility is based on childbirth or childrearing, and the exclusion of single fathers raising children due to circumstances beyond their control—the program places a significant burden on an already strained state budget.

The Hungarian government has set a 3.7% deficit target for the 2025 budget[3]. However, this must be viewed in light of the fact that, in recent years, government projections have consistently underestimated the deficit. In contrast, the European Union forecasts a 4.6% deficit for Hungary in its latest medium-term convergence report[4]. For 2026, an election year, the government plans for a slightly lower deficit of 3.6%. This would require either spending cuts or revenue increases to meet the target. The newly announced package of tax measures runs counter to these objectives.

It is therefore no coincidence that the European Union projects a 4.1% deficit for 2026. In nominal terms, the HUF 655 billion tax relief package is expected to increase the 2026 budget deficit by approximately 15%.

While the tax exemption may support families, improve living standards, and stimulate consumption, its long-term sustainability, social fairness, and macroeconomic implications remain uncertain. The positive effects are primarily expected in terms of encouraging childbirth and enhancing the financial flexibility of households. Should economic growth remain robust, a portion of the lost revenue could be recouped through increased consumption and resulting tax receipts.

[1] Assumptions: It is assumed that the income quintiles of mothers with two children correspond to the overall population income quintiles. (Source: Hungarian Central Statistical Office – https://www.ksh.hu/ksh-monitor/keresetek.html)

[2] Proportion of increased income allocated to consumption expenditure, by quintile: 1. quintile – 100%, 2. quintile – 90%, 3. quintile 80%, 4. quintile 60%, 5. quintile 20%.

[3] https://www.parlament.hu/irom42/09894/09894.pdf

[4] https://economy-finance.ec.europa.eu/document/download/c83afff2-0248-4189-ac54-66e716e43509_en?filename=MTFSP_2025_HU.pdf