Construction output has been on a steady decline over the past two years, and this unfavorable trend persisted into the first quarter of 2025. Amidst weakening demand, the number of active firms in the sector has also decreased, while producer price inflation has begun to ease. Industry stakeholders currently see no signs of an imminent turnaround, although the medium-term growth prospects for the sector remain positive.

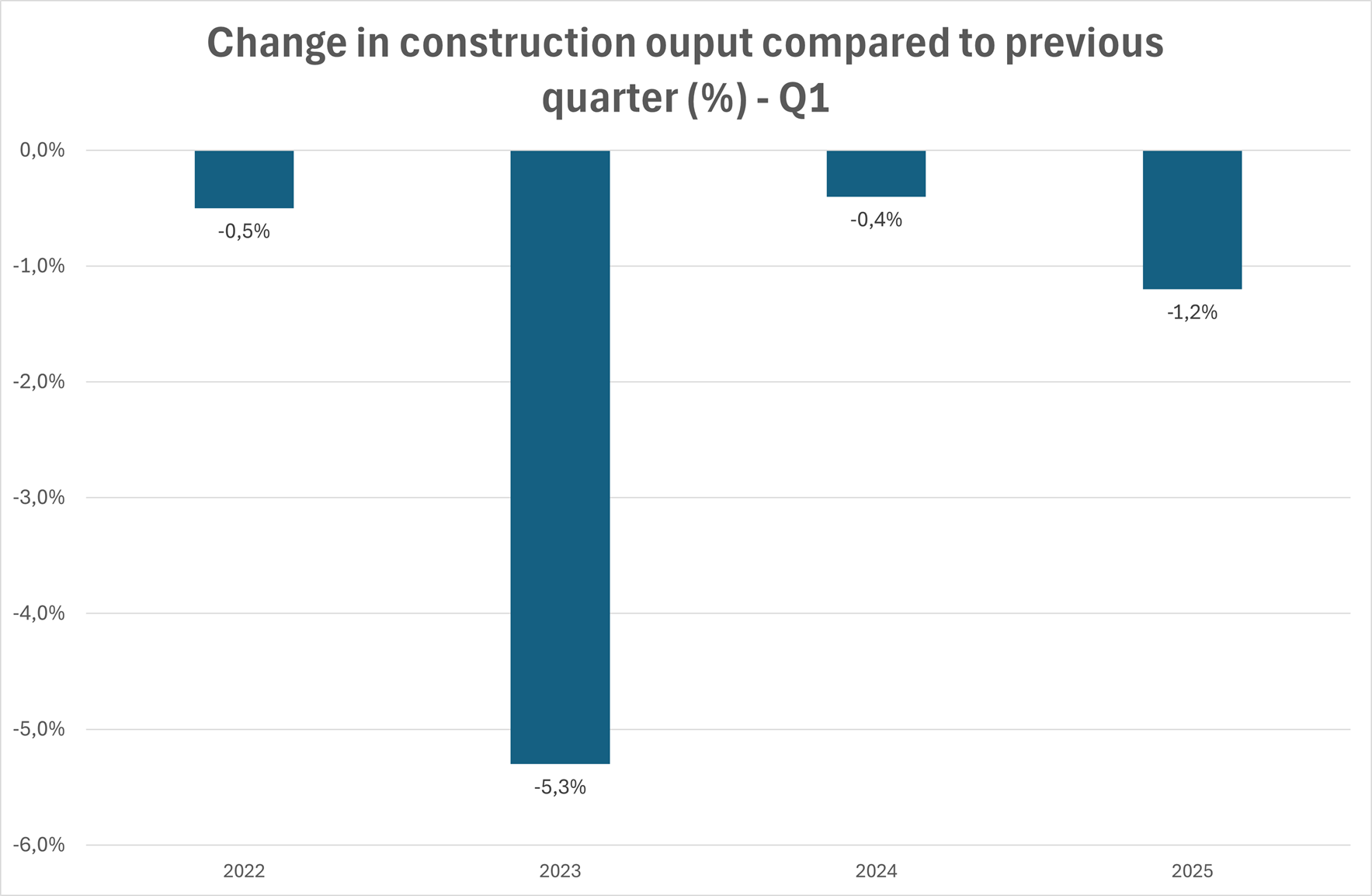

The growth cycle of the construction industry came to an end in 2022. Sector output contracted significantly in 2023 by 5.3%, followed by a more modest decline of 0.4% in 2024. The start of 2025 has offered little relief: production volume in the first quarter fell by 5.7% year-on-year. However, the building construction segment (residential and non-residential) held steady, showing virtually no change from the same period a year earlier. In contrast, civil engineering (infrastructure and other large-scale projects) saw a pronounced decline of nearly 9%.

The industry’s own investment activity has been decreasing for three consecutive years. A particularly concerning indicator for the near term is the volume of new contracts signed in the first three months of 2025, which was 18% lower than in the same period of 2024. Although the total order book held by construction companies at the end of March was 3.8% higher than a year earlier, a large proportion of these contracts are longer-term in nature and will not substantially contribute to output in 2025. From this perspective, the civil engineering segment appears better positioned, as a greater share of its contracts is expected to materialize within the current year.

The accompanying chart illustrates the annual change in Hungary’s construction output over the period from 2022 through the first quarter of 2025. Negative values indicate year-on-year contractions. The most significant decline occurred in 2023, when output fell by 5.3%. The figure for the first quarter of 2025 is preliminary.

Source: GKI Economic Research Co., based on data from the Hungarian Central Statistical Office (KSH).

The number of active construction firms, as well as the rate of new company formations, declined in both 2023 and 2024. Due to the high prevalence of dormant entities and project-based firms within the sector, the number of genuinely active enterprises was estimated at around 65,000 by the end of 2024. This downward trend in firm numbers continued into the first quarter of 2025, though the number of new registrations rose by 8% year-on-year.

While rising construction material prices, uncertainty surrounding energy costs, and continued wage pressures have kept producer inflation elevated, weakened demand has limited firms’ pricing power. Producer prices rose by an average of 16% in 2023, slowed to 6% in 2024, and increased by 5.4% in the first quarter of 2025. A significant deceleration in the pace of price growth is not expected over the course of the year.

Over the past two years, insufficient demand has emerged as the most critical constraint on sector output. According to a GKI survey conducted in April, more than half of respondents cited demand weakness as a key obstacle. Roughly a quarter also reported challenges related to labour shortages, delayed client payments, and broader financial difficulties. By contrast, in the sector’s stronger years (2021–2022), labour scarcity was the leading constraint—mentioned by over 50% of respondents—while demand concerns affected only about one in five firms. The sector’s sentiment, as measured by GKI’s construction confidence index, remained broadly stable throughout 2024 but showed signs of deterioration in early 2025. After peaking in January, the index declined steadily through May, reaching a four-year low. Current business expectations suggest no imminent recovery. For 2025, GKI forecasts flat construction output compared to 2024, though downside risks remain considerable.

The quality of construction firms’ loan portfolios deteriorated steadily during 2022–2023, with only marginal improvement in 2024, according to data from the National Bank of Hungary (MNB). Mounting market pressures have led to a rise in payment arrears across the value chain, exacerbating financial vulnerabilities and undermining the sector’s overall stability. The financing of domestic construction projects—particularly those commissioned by the public sector—remains heavily reliant on EU funds. Delays and partial disbursements of resources from the 2021–2027 EU financial framework have further strained the industry.

Despite current headwinds, the construction sector holds several sources of growth potential over the next 3–4 years. Government stimulus plans, including housing construction and renovation programs, are expected to bolster activity mid-term. Additional upside may come from energy-efficiency investments, which could stimulate demand for building upgrades. Publicly funded infrastructure projects—especially in transportation—could also create new opportunities for firms across the sector.

Advances in technology and digitalization may improve operational efficiency and competitiveness, supporting long-term expansion. However, multiple structural risks remain. Geopolitical uncertainty, volatile energy prices, growing labour shortages, and upward wage pressures all pose significant challenges. Furthermore, uncertainty around future interest rate developments could weigh on investment decisions. New regulatory compliance requirements could increase administrative and financial burdens on construction firms. The overarching challenge for all participants across the construction value chain will be to drive efficiency improvements in an increasingly complex and competitive environment.