The May of 2025 has marked an acceleration in changes within the global economy. Tensions in the Middle East have escalated over recent months, while two nuclear powers—India and Pakistan—were briefly drawn into direct confrontation over terrorism and disputed water usage rights. Existing geopolitical frictions have contributed to volatile raw material prices and disruptions in trade and supply networks. The resurgence of trade wars is slowing global economic growth and the expansion of international commerce. In Europe, a radical transformation of the energy market is underway, which, while gradually reducing dependence on Russian energy sources, is also pushing up long-term costs.

In May 2025, trade tensions between the European Union and the United States intensified to a concerning degree. Last week, the U.S. President announced a potential 50% tariff on imports from the EU, effective June 1st, though this measure has been suspended for one month. Should the European Union respond with retaliatory measures, it may further escalate the trade conflict and significantly impact EU export sectors. Hungary—as an export-driven EU member state particularly reliant on the automotive industry—is especially vulnerable to declining global demand and supply chain disruptions.

U.S. foreign policy has shifted toward stronger national interest enforcement. This pivot has resulted in rising tensions with several former partners and economic competitors, leading to a reduction in foreign trade and economic growth. Over time, some of these effects may be mitigated as countries displaced from the U.S. market seek closer economic ties with the EU. This development also implies that the European Union will eventually need to shield itself from a potential influx of cheap goods—primarily from China—a trend already beginning to manifest.

From a European perspective, the economic consequences of Russia’s war against Ukraine remain highly significant. Higher energy prices, the effects of sanctions, and the compulsion to increase defence spending are all collectively dampening growth prospects. While lifting sanctions could enhance economic growth forecasts for the EU—especially in Central and Eastern Europe—this impact is likely to be limited due to the ongoing transition away from Russian energy sources. The EU’s sharply increased defence expenditures are expected to make only a moderate contribution to economic growth and simultaneously divert resources from other, more growth-oriented sectors.

The Hungarian government continues to pursue strong relations with Eastern countries (and the United States). In recent years, Hungary has attracted most of its foreign investments from China and South Korea. The outlook for Hungary’s economy remains closely tied to the automotive industry and, by extension, to global demand for battery industry products and relevant EU regulations. However, the prospects for these sectors remain unfavourable.

Energy supply security and cost are of strategic importance for Hungary. Currently, the TurkStream pipeline ensures gas supplies, also enabling Hungary to benefit economically from its role as a transit country within the region. However, should the EU proceed with further drastic restrictions on Russian energy imports—currently planned for implementation from 2026—it would pose a significant cost burden to the Hungarian economy.

As an open, export-oriented economy, Hungary is highly exposed to these global developments. The EU–U.S. tariff dispute, the EU’s evolving energy policy, and the restructuring of global competition in the automotive sector all exert direct or indirect influence on Hungary’s export potential, energy supply, and industrial base. Consequently, Hungary’s economic policy has limited manoeuvrability in this environment. In the period ahead, the ability to flexibly adapt to external shocks, capitalize on emerging market niches, and advocate for national economic interests within the EU in an effective and constructive manner will be of key importance.

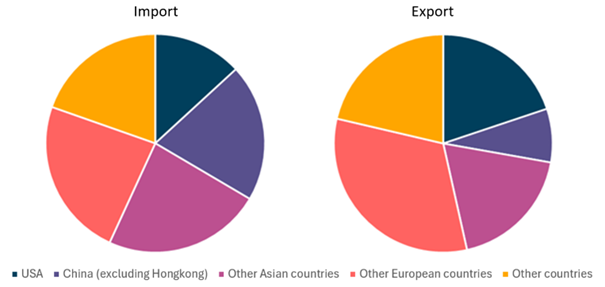

Breakdown of the European Union’s Imports and Exports by Partner Country/Region (2024)

Source: GKI calculations based on Eurostat data