Industrial output in Hungary decreased for the second consecutive year, with a 5.5% drop in 2023 followed by a further 4% decline in 2024. Both domestic and export sales contracted over the period. Industrial GDP also fell, with total industry output shrinking by 4.4% and manufacturing by 3.7% in 2023; in 2024, the respective declines were 3% and 4.4%. The downturn reflects broader European trends and the structural weaknesses of Hungary’s industrial development. As a result, output in motor vehicle manufacturing fell by 13.3% in 2024, while battery production plummeted by 22.4%, largely due to declining demand from European factories. These two subsectors were the primary drivers of the industrial slowdown[1].

In the first quarter of 2025, industrial production declined by 4.4%. Export sales, which account for 63% of total sales, remained stagnant, while domestic sales, representing 37%, decreased by 3%. Production fell in nine of the thirteen subsectors within manufacturing, with the most significant decline—25%—recorded in the manufacture of electrical equipment. Output in the largest subsector, motor vehicle manufacturing, fell by 3.8%. Only the manufacture of computer, electronic, and optical products showed meaningful growth[2].

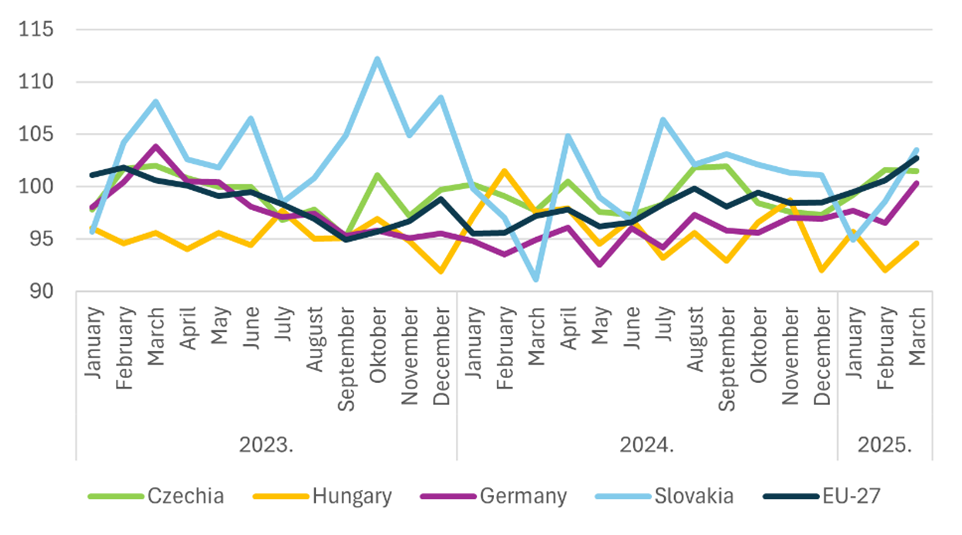

Since early 2023, Hungary’s industrial production performance has been persistently weaker than the EU average, with only a few exceptions. By the end of the first quarter of 2025, industrial production had entered a growth trajectory across the EU as a whole, including in Germany, as well as in the automotive-heavy economies of the Czech Republic and Slovakia. In contrast, production in Hungary continued to decline.

Volume Index of Industrial Production in Hungary and the EU

(Same period of the previous year = 100%) Source: Hungarian Central Statistical Office (KSH), Eurostat

Source: Hungarian Central Statistical Office (KSH), Eurostat

Outlook Remains Bleak for Hungarian Industry. While European industry is gradually recovering from the inflationary shocks following the COVID-19 pandemic and the energy crisis, a full-scale rebound in the automotive sector is expected to take significantly longer. The 25% tariff on cars imposed by former U.S. President Donald Trump could jeopardize this fragile recovery in the EU—unless an agreement is reached with the United States on the matter.

The uncertainty surrounding tariffs (with Trump threatening to raise duties on EU goods to as high as 50%, even as the International Trade Court has ruled many new tariffs unlawful—though notably not the 25% automotive duty) has created an unpredictable economic environment[3]. This has led to postponed investments and delayed production expansions, affecting not only the industrial sector but also key related industries such as logistics and energy.

In Hungary, business sentiment remains pessimistic, and current order volumes are significantly lower than a year ago. Furthermore, the sources of future industrial growth are also in question. Employment in the industrial sector declined by 1.5% in 2024, while manufacturing employment dropped by 1.8%. According to business surveys conducted by GKI Economic Research Co., industrial firms are anticipating further job cuts. While this could theoretically improve productivity, it would require investment—yet investment in manufacturing fell by 4.7% in 2023 and by a further 14.2% in 2024.

Moreover, current investment activity is not geared toward capacity expansion. The majority of respondents in GKI’s business surveys cited replacement of outdated equipment as their primary investment motive. There is, as of now, no indication of significant investments aimed at expanding production or developing new products. This suggests continued contraction—or at best, stagnation—in Hungarian industry.

No substantial improvement is expected in Hungarian industrial performance during the first half of 2025. As conditions gradually improve in Hungary’s key export markets, the domestic contraction may eventually bottom out. Underutilized capacities could support some degree of growth. A few large-scale investments may also contribute positively once they enter the production phase—namely, the CATL and BMW plants in Debrecen and the BYD factory in Szeged. However, the timing and impact of these developments depend heavily on improving market conditions across Europe. All things considered, a slow recovery in industrial output could begin in the second half of 2025.

[1] https://www.ksh.hu/stadat_files/ipa/hu/ipa0002.html

[2] https://www.ksh.hu/gyorstajekoztatok/ipa/ipa2503.html

[3] https://www.reuters.com/business/us-ruling-that-trump-tariffs-are-unlawful-stirs-relief-uncertainty-2025-05-29/