Following our analysis of productivity trends in manufacturing, construction, trade, and the ICT sector[1], we now turn our focus to financial and insurance services. In 2023, the financial and insurance sector accounted for an average of 4.6% of GDP across the European Union. This share varied significantly, from 2.7% in Slovakia to 4.1% in Hungary and up to 5.1% in Poland[2].

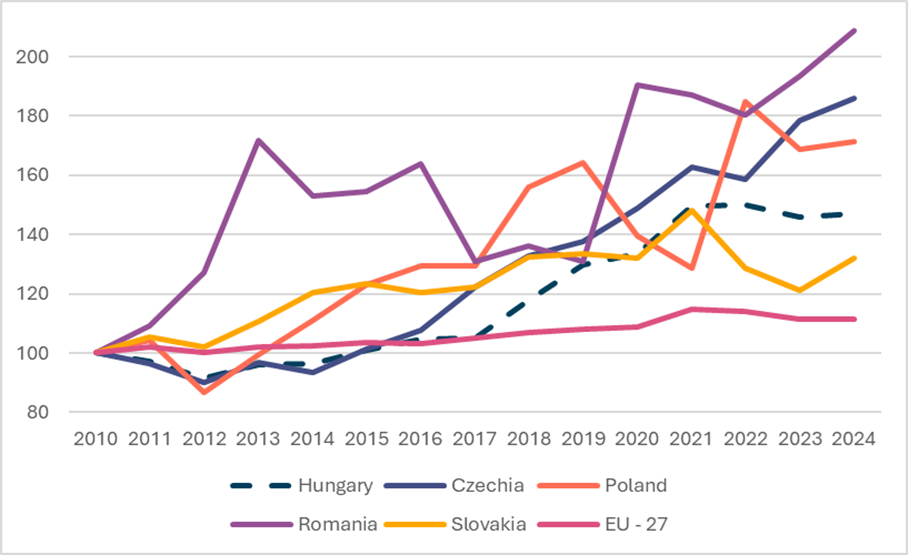

Between 2010 and 2024, labour productivity in the EU’s financial and insurance sector rose by 11%. However, countries in the Central and Eastern European region far outpaced this growth. Even Slovakia, the region’s weakest performer, recorded a 32% increase by 2024. Hungary reached a 47% improvement, while Poland (71%) and the Czech Republic (86%) posted even stronger gains. Romania led the region with a remarkable 109% increase in productivity over the same period.

Labour Productivity in the Financial and Insurance Sector in the V4 Countries, Romania, and the EU-27, 2010–2024 (2010 = 100%)

Source: Eurostat

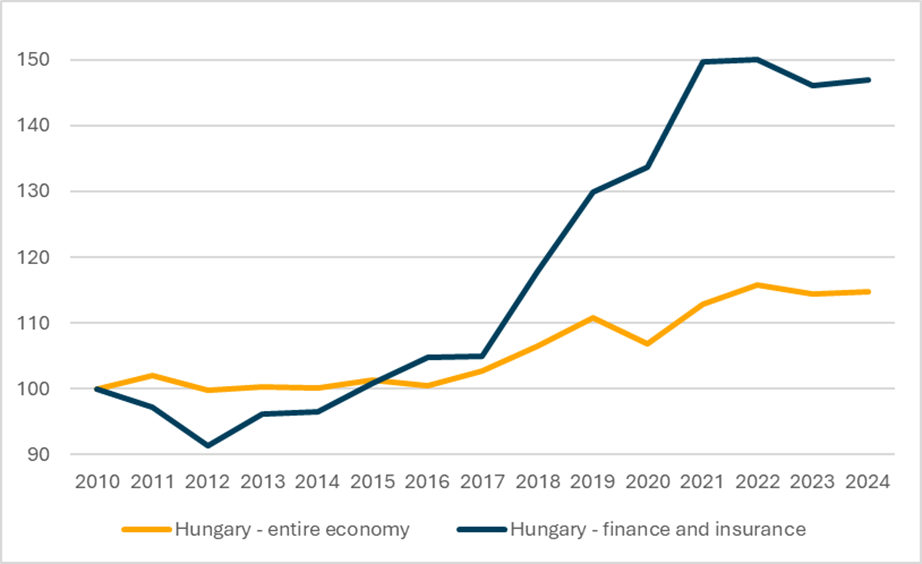

In Hungary, labour productivity in the financial and insurance sector declined in the early 2010s, only surpassing 2010 levels by around 2016–2017. However, this was followed by a period of strong, dynamic growth, with productivity improving by more than 40 percentage points by 2021.

Since then, progress has stalled, and a slight decline has been observed. A key factor behind this reversal has been the sector-specific windfall taxes, which have diverted resources away from development and investment.

Even so, thanks to the earlier gains, the sector’s overall 47% productivity growth between 2010 and 2024 significantly outperformed the national average of 15%. As a result, the financial sector has been a positive contributor to Hungary’s aggregate productivity performance—especially when compared to the manufacturing sector, where productivity growth stood at a modest 8%, thus dragging down the national figure.

Changes in Labour Productivity in the Hungarian National Economy and the Financial & Insurance Sector, 2010–2024 (2010 = 100%)

Source: Eurostat

Since 2010, Hungary’s banking and insurance system has undergone significant digital transformation. The proliferation of mobile banking apps, the expansion and improved quality of online services, and the reduction in the number of physical bank branches have all contributed to a decline in the demand for on-site personnel. However, rising administrative requirements in the sector have offset these labour savings, resulting in a net increase in employment.

Between 2010 and 2024, the number of employees in the sector rose from 103,000 to 112,000—an 8.7% increase[1]. In contrast, total national employment grew by 20% over the same period. This indicates that while the broader economy expanded primarily through extensive growth, the financial and insurance sector achieved gains almost exclusively through intensive growth.

Aiding this shift was the near-elimination of foreign currency-denominated loans in the household segment, reducing the sector’s exposure to exchange rate-related defaults. At the same time, improved customer service and more sophisticated risk assessment practices helped mitigate other types of losses. Today, most insurance contracts are indexed to inflation, preserving the real value of insurance revenues and thereby boosting operational efficiency for insurers.

However, non-bank-owned leasing firms and other financial enterprises—key players in the micro-finance market—have not benefited from the same flexibility. Their one-sided revenue structures and reliance on subsidies make them particularly vulnerable to tax burdens. Sector-specific levies directly constrain their lending capacity, threaten their sustainability, and undermine their efficiency.

Over the past fifteen years, the financial and insurance sector has demonstrated exceptional productivity growth, driven by digitalisation, operational efficiency, and improved risk management. This has made a significant contribution to national economic performance. In Hungary, the sector’s 47% productivity increase has more than tripled the national average of 15%.

Despite these advances, the sector has faced a growing tax burden in recent years—through instruments such as the bank levy, financial transaction tax, windfall profit tax, insurance tax, and, most recently, mandated “voluntary” fee reductions. These measures have squeezed corporate profitability. While productivity has continued to rise in the short term, declining profitability threatens the sector’s long-term growth potential, which could ultimately prove counterproductive for both the market and the state.

[1] Previous articles: https://gki.hu/language/hu/2024/10/31/stagnalas-kozeleben-a-munkaero-termelekenysege-a-feldolgozoiparban-magyarorszagon/ and https://gki.hu/language/hu/2025/04/08/a-kereskedelemben-6-szor-gyorsabban-nott-a-termelekenyseg-2010-ota-mint-a-feldolgozoiparban/

[2]Source:https://ec.europa.eu/eurostat/databrowser/view/nama_10_a64__custom_16285228/default/table?lang=en

[3] Source: https://www.ksh.hu/stadat_files/mun/hu/mun0009.html