In recent months, GKI Economic Research has conducted a comprehensive series of analyses examining labor productivity across various sectors of the Hungarian national economy. The findings reveal a sobering reality: Hungarian companies consistently lag behind their regional competitors in terms of labor productivity—particularly in sectors that are prioritized by government economic policy.

This raises important questions regarding the effectiveness of the current legal and economic incentives, as well as the structure of public support mechanisms. The data suggest that these frameworks may require fundamental reassessment. Enhancing productivity is not only a matter of short-term economic gain, but a prerequisite for sustainable long-term competitiveness.

Bringing about structural improvements in this area should be considered a priority for policymakers committed to driving meaningful economic progress.

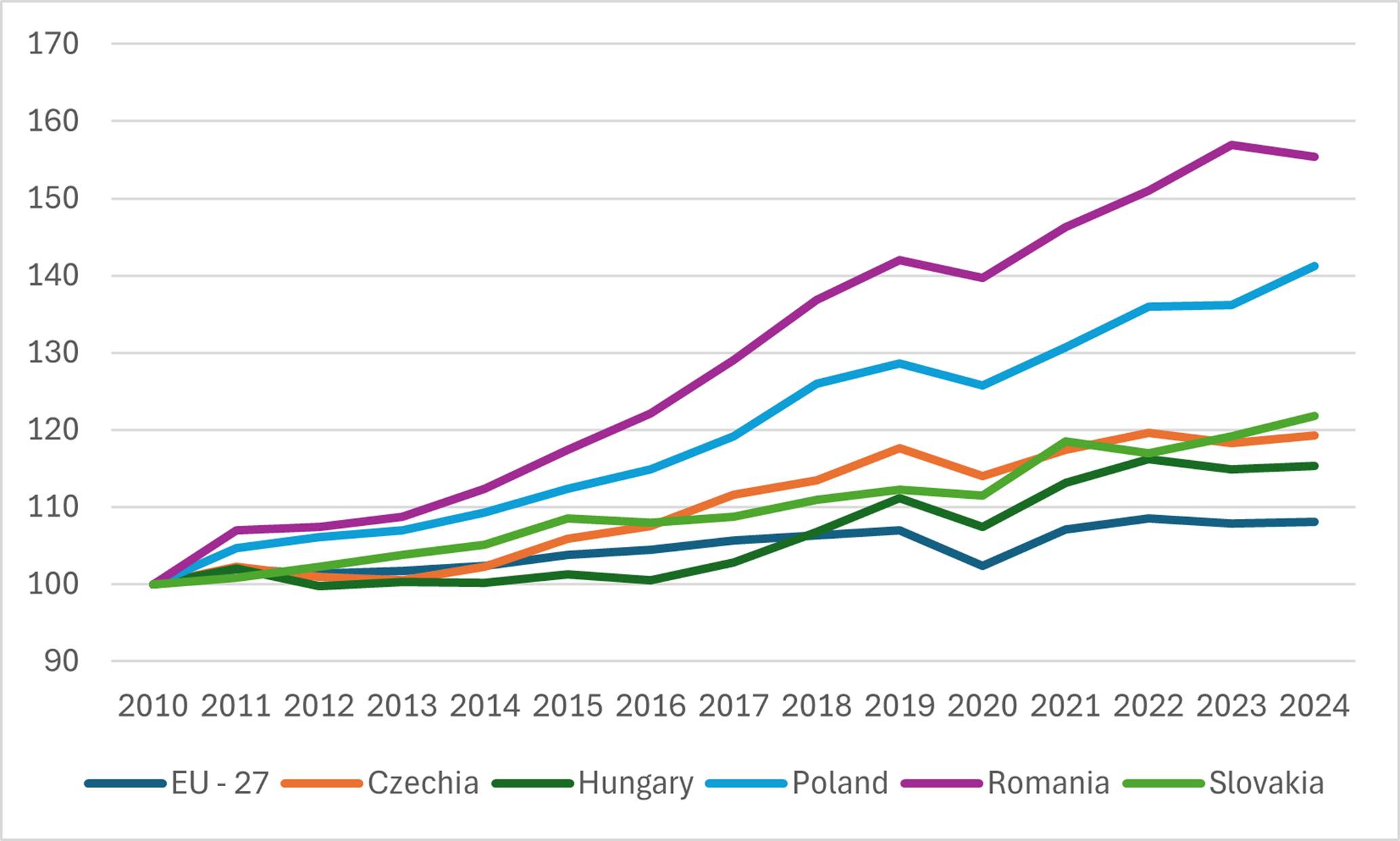

Labor Productivity in the Visegrád Four, Romania, and the EU-27, 2010–2024 (2010 = 100) Source: Eurostat

Source: Eurostat

From an international comparative perspective, the countries of the region (the Visegrád Four and Romania) have followed broadly similar trajectories in terms of productivity growth since 2010. However, the magnitude of growth varies significantly. All countries in the region comfortably outpaced the EU average: while the EU-27’s productivity rose by just under 10%, the regional average was roughly twice as high—and in some cases, even quintupled the EU’s pace.

Romania and Poland emerged as clear outperformers, achieving productivity gains of 55% and 41%, respectively. By contrast, the Czech Republic and Slovakia delivered more modest increases of around 20%.

Hungary, however, recorded the weakest performance among the countries analyzed, with a cumulative productivity growth of just 15%. Notably, this improvement was concentrated between 2016 and 2022; before and after this period, the country’s labor productivity either stagnated or declined.

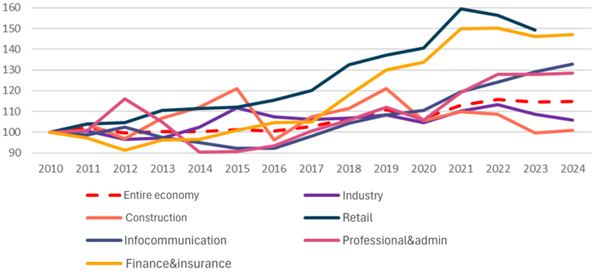

Looking at sectoral structure, Hungary’s leading sectors in terms of productivity gains were trade and financial-insurance services, each posting around 50% growth. Information and communication, along with professional, scientific, and administrative services, also showed strong performance, with growth rates of 30–32%.

In stark contrast, the overall national average of 15% was significantly pulled down by the manufacturing sector, which registered a meager 5% increase, and the construction sector, which showed no growth at all. Strikingly, the sectors driving productivity improvements account for just 30% of GDP, while the slower-developing sectors make up 26%. Despite this imbalance, a disproportionate share of fiscal subsidies has flowed into the latter group—particularly to multinational assembly plants.

Productivity by Sector in the Hungarian National Economy, 2010–2024 (2010 = 100)

Source: Eurostat; (Note: the above categories do not cover all economic activities)

In recent years, Hungarian economic policy has placed strong emphasis on large-scale stimulus programs—most notably, on investments in the manufacturing sector and the funding of major infrastructure and strategic projects within the construction industry.

While this influx of financial resources can support short-term development in certain sectors, its long-term impact on productivity is contingent upon whether companies are encouraged to improve efficiency, pursue innovation, and adopt a more cost-conscious approach to operations.

In light of this, it would be more rational to consider reallocating future subsidies toward areas where Hungary holds a comparative advantage and where long-term, sustainable growth is more likely. This would mark a departure from current practices, which continue to favor industries heavily dependent on imported raw materials, energy, and foreign labor—such as battery production and automotive manufacturing.

Additionally, there is a clear need to further refine the set of economic policy tools. Introducing more sophisticated, predictable, and effective incentive schemes—ones that are better aligned with existing comparative and competitive advantages and that pay greater attention to the needs of domestic small and medium-sized enterprises—could provide a more solid foundation for sustained productivity growth.