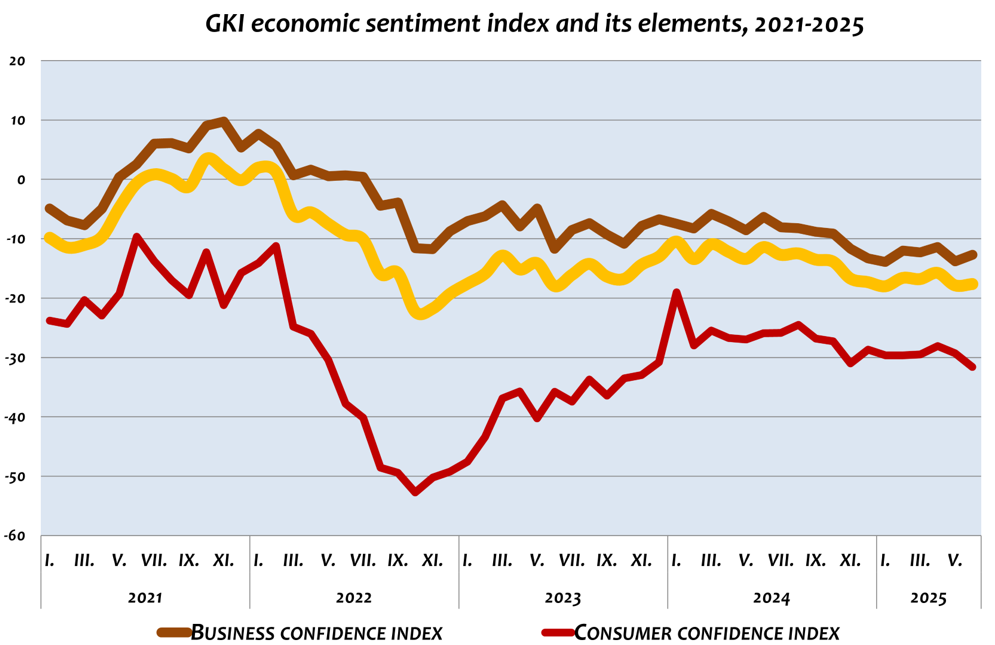

According to the latest survey conducted by GKI Economic Research Co. with the support of the European Union, Hungary’s business sentiment index remained flat in June. While consumers grew slightly more pessimistic compared to May, businesses expressed a modest uptick in optimism regarding the near-term economic outlook. As a result, the composite GKI Economic Sentiment Index showed no net change for the month.

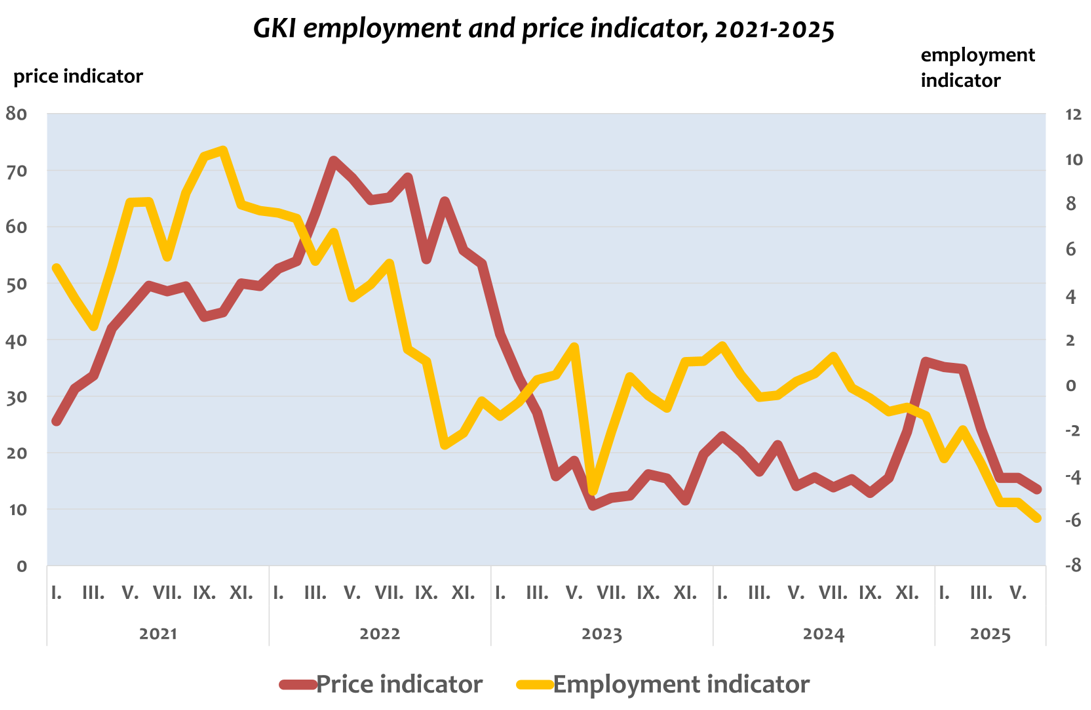

Corporate hiring intentions remained broadly stable, with only marginal variation from the previous month. Meanwhile, companies’ aggregate expectations for future price increases fell to their lowest level in eight months – marking a continued decline in inflationary pressures from the corporate side.

Following a decline of just over two points in May, GKI’s Business Confidence Index edged up by one point in June, returning to its level from three months earlier. The moderate improvement was driven primarily by a notable recovery in industrial sentiment, where the sector’s confidence index rose by three points compared to the previous survey. By contrast, sentiment in the trade sector remained unchanged, while the construction confidence index dropped by three points and the services sector index fell by nearly two. Despite these sectoral shifts, the overall outlook remained broadly stable: construction continues to be the most cautious segment of the economy, whereas business services remain the most optimistic.

GKI’s June survey reveals that corporate employment expectations remained practically unchanged compared to the previous month. The only significant deterioration occurred in the construction sector, while expectations in all other sectors remained stable. Over the next three months, 8% of companies plan to increase headcount, while 12% anticipate staff reductions—compared to 9% and 12%, respectively, in May.

Perceptions of the predictability of the business environment also remained largely unchanged in June, with the construction industry again reporting the most negative assessments.

The price expectations indicator – summarizing corporate pricing plans into a single measure – declined for the sixth consecutive month, reaching its lowest point in eight months. Apart from the retail sector, all industries reported reduced intentions to raise prices. For the coming quarter, 17% of firms expect to increase prices, while 8% plan to reduce them. A month earlier, these figures stood at 20% and 8%, respectively.

Consumer confidence saw a noticeable decline in June. The GKI Consumer Confidence Index fell by two points, dropping to its lowest level since late 2022. Households perceived their financial situation over the past 12 months as having deteriorated slightly, though expectations for the coming year showed a modest improvement. However, expectations regarding the national economy worsened further, and households’ willingness to spend on major consumer goods remained unchanged. Inflation expectations ticked up marginally, while concerns over rising unemployment grew more pronounced.

The underlying data and charts are provided in the attached Excel file.

Methodological Note:

GKI Economic Research Co. calculates its Economic Sentiment Index in line with the methodology of the European Commission. The index reflects both business and consumer expectations, combining the Business Confidence Index and the Consumer Confidence Index as a weighted average.

The Business Confidence Index is the weighted average of sentiment indicators from the industrial, retail, construction, and business services sectors.

The Employment Indicator represents the difference between the proportion of companies planning to increase vs. decrease staffing levels over the next three months.

The Price Expectations Indicator is the difference between the proportion of companies planning to raise vs. lower their selling prices in the next quarter.

The Consumer Confidence Index is the arithmetic average of balance indicators derived from household responses to questions regarding their past 12-month financial situation, financial expectations for the next 12 months, the expected economic situation of the country, and prospects for purchasing durable goods.

GKI reports seasonally adjusted data, filtering out fluctuations caused by seasonal factors—such as increased demand before Christmas or reduced production during the summer holiday period—using standard statistical techniques.

Download full study