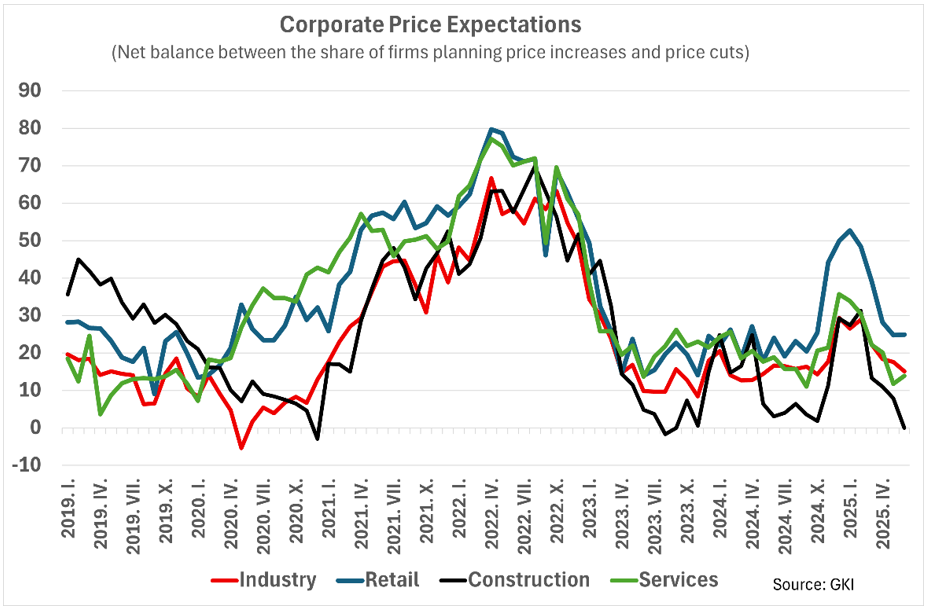

So far in 2025, inflationary intentions across several sectors of Hungary’s business landscape have markedly weakened. By June, corporate expectations for price increases had fallen to an eight month low. Nonetheless, with the exception of the construction sector, pricing ambitions in all major industries remain close to their long-term averages. This suggests that, despite recent moderation, inflationary pressure is likely to persist in the short term.

Can firms become allies in the fight against inflation?

For decades, GKI Economic Research Co. has conducted monthly surveys of Hungary’s business sector, adhering to the methodology of the European Commission. These surveys span industry, construction, retail, and business services. Among other indicators, they regularly assess corporate pricing expectations. Given the sharp inflationary surge that gripped Hungary’s economy in 2022 and 2023, followed by a notable slowdown in price growth in 2024: it is only natural to ask: What do firms expect now? What do their pricing plans reveal about the economic outlook? The government’s priority is clear: to rein in inflation swiftly, or at the very least, to keep it under control. But the question remains: can the corporate sector be a willing partner in this effort?

What do past data reveal?

In recent years, Hungary’s economy has been hit by a series of external shocks. The first was the Covid-19 pandemic, which – at least in the short term – led pricing strategies across sectors onto divergent paths. The outbreak triggered a sharp rise in price expectations in the retail and services sectors, while those in industry and, particularly, construction climbed only later. Industrial price expectations hit their lowest point in June 2020, while those in construction bottomed out only in January 2021. As awareness of the energy crisis sparked by Russia’s aggression against Ukraine grew, pricing intentions rose steadily across all four sectors. This was further amplified by the post-pandemic rebound. But the surge in energy prices marked a turning point: inflationary intentions among firms surged dramatically. Starting from mid-2022, however, as the initial shock wore off, price expectations began to recede. Between mid-2023 and late 2024, pricing sentiment entered a relatively calm phase, with no clear direction emerging. By late autumn 2024—likely reflecting growing economic uncertainty—price expectations began to inch upward again, most notably in retail, though less so in the other sectors. In the first half of 2025, however, pricing ambitions weakened almost continuously. In construction, waning demand has become a dominant constraint. Delays and cancellations in public infrastructure projects, a trough in new home construction, and a slowdown in renovations all help explain the more cautious pricing stance. In retail, where price expectations had risen most sharply in 2024, the subsequent decline appears to be a natural correction—one further reinforced by government measures aimed at curbing price growth. Business services also underperformed in early 2025, making their softer pricing outlook unsurprising. Meanwhile, a significant share of industrial output is sold abroad, where demand remains volatile—adding further unpredictability to firms’ pricing strategies.

What lies ahead?

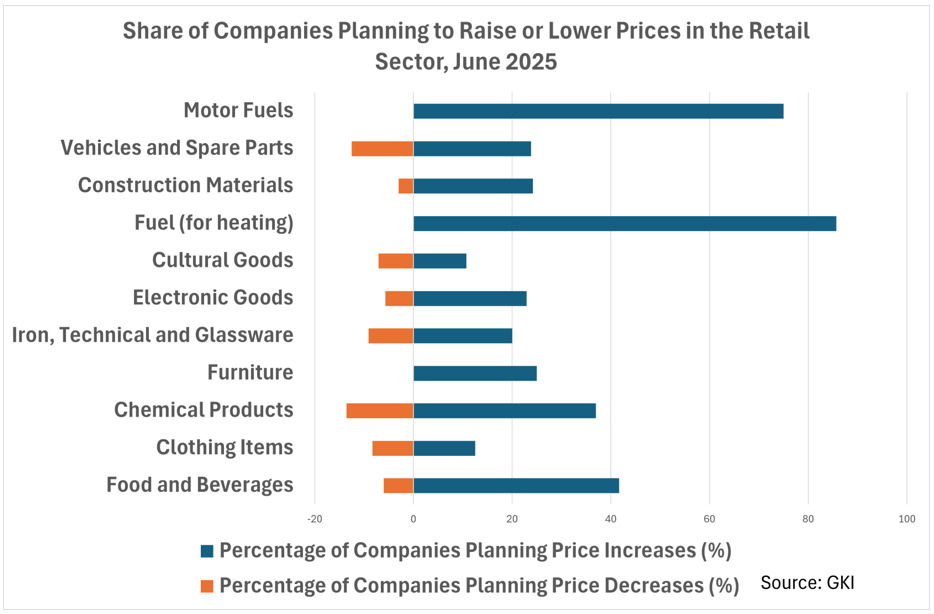

As of June 2025, across the four main sectors combined, 17% of firms were planning to raise prices over the next three months, while 8% anticipated cutting them. In construction, the proportion of businesses expecting price increases or decreases was evenly split at 14%—an indication of muted inflationary pressure in the sector, largely due to subdued demand. In industry, 13% of firms planned price hikes, compared to 5% expecting reductions. In business services, the figures were 15% and 6%, respectively. The most troubling news for consumers comes from the retail sector, where pricing pressure remains strongest: 27% of respondents planned to raise prices, while only 8% intended to lower them. This is hardly surprising. Retailers are still seeking to offset losses caused by government-imposed price margin caps and sector-specific taxes, all while facing persistent upward pricing pressure from their suppliers.

The survey responses leave little doubt: in the fuel and energy segments, a decisive majority of firms expect to raise prices in the near future. The outlook is similarly inflationary for everyday consumer goods, with food, beverages, and household chemicals all facing broad-based price expectations on the upside. With the exception of apparel and cultural goods, price increases are anticipated across nearly all other product categories, with those expecting to raise prices clearly outnumbering those planning cuts. Corporate expectations suggest that while weak demand is acting as a brake on pricing ambitions in several sectors, cost-side pressures remain stubbornly entrenched. Elevated energy prices, continued disruptions and inefficiencies in supply chains, rising wage costs, and increasing tax burdens are all contributing to a landscape in which inflationary momentum may be down—but it is far from gone.