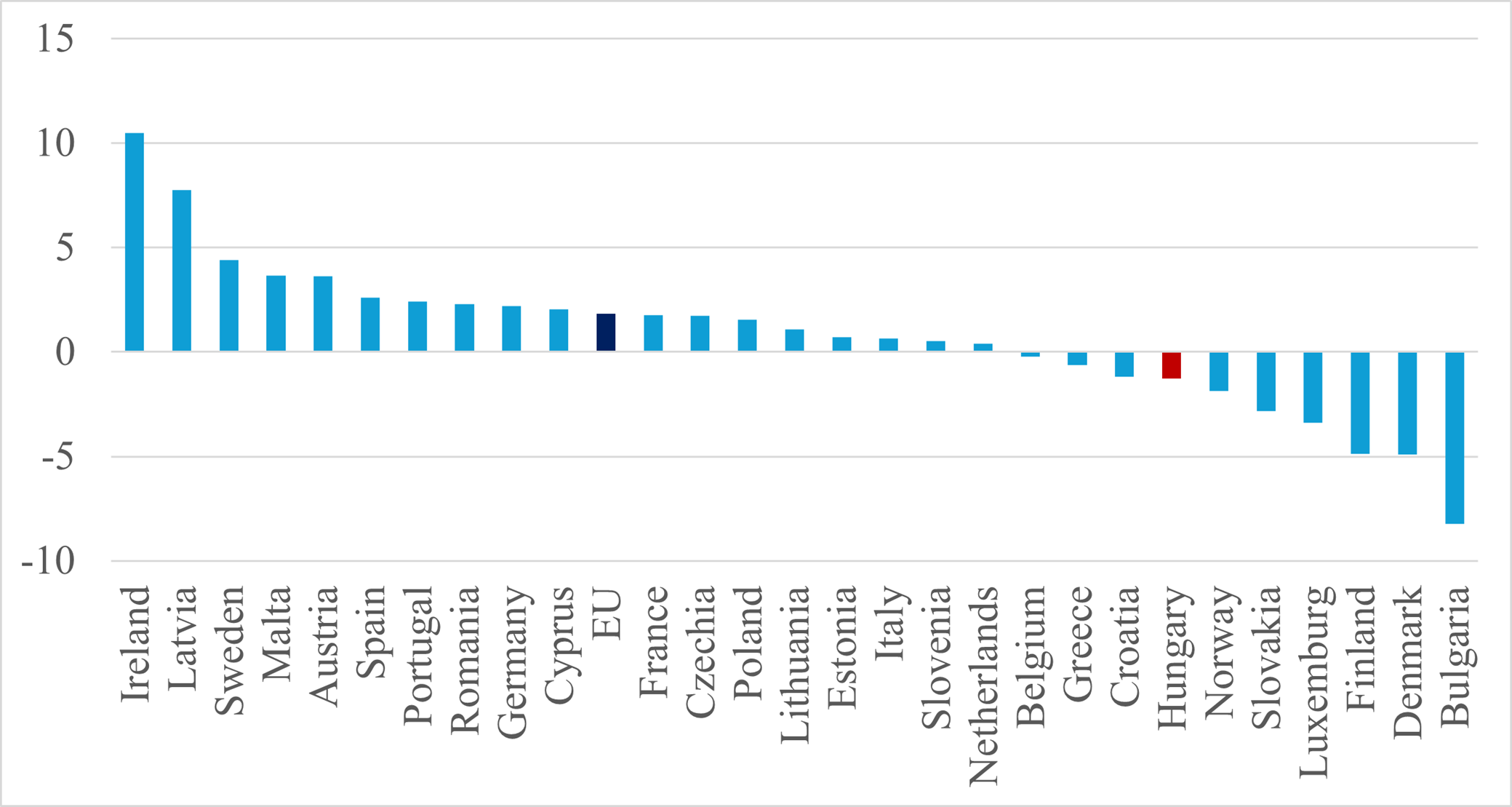

In July 2025, industrial output in the EU rose 1.8% compared with the same month in 2024. Germany’s industry, which only returned to growth in May, expanded by 2.2% year on year in July – a welcome sign for Hungarian manufacturers, given that they share some of the same markets and supply many German factories. In contrast, Hungary’s industrial production fell by 1.3% in July, the 7th largest decline in the EU.

Industrial Production in Select EU Countries

Year-on-Year Change, July 2025 (%)

Source: Eurostat[1]

In the first eight months of 2025, Hungary’s industrial output fell 7.3% compared with the same period last year (a seasonally and calendar-adjusted decline of 2.3%). Exports, which account for 64% of total sales, slipped 1.3%, while domestic sales, representing 36%, fell 5.3%.[2] The steepest drops were seen in coke production and oil refining (-20%), chemicals (-14.4%) and textiles (-11.2%), though mining (-8.5%) and electrical equipment – including battery manufacturing – (-8.3%) also contracted. Among the 15 sectors monitored by the Hungarian Central Statistical Office, output fell in nine and rose in five. Within manufacturing, the heavy-weight vehicle industry was largely stagnant in July. Reports from Hungarian car factories point to reduced shifts and layoffs, while the expected boost from new large-scale plants is likely to remain modest this year.

Output fell in 12 manufacturing sub-sectors in the first seven months of the year. Electronics, however, grew by 8.2%, giving a notable boost to overall performance. Production also rose in the wood, paper and printing industries (3.1%) and in the electricity sector (1.9%).

The main drag on production remains weak demand, according to GKI’s business surveys. Statistics from the Hungarian Central Statistical Office (KSH) confirm the picture: both domestic and export sales fell in the first seven months of 2025, by 3.7% and 1.5%[3] respectively. Short-term prospects remain grim: in July, order books across the sectors tracked by the KSH were 7% smaller than a year earlier. Constraints also come from the supply side. While respondents to GKI surveys once cited labour shortages as the chief obstacle to growth, this factor has recently receded, and where it persists, it is a shortage of skilled rather than sheer labour. Employment in industry fell 1.5% in 2024 and has dropped a further 3% in the first three quarters of 2025[4].

The picture is similar on the capacity side. Manufacturing investment plunged 17.4% in the first half of 2025, although several large-scale projects (including new plants by BMW, BYD and CATL) are underway and could give the sector a boost once activated. In June, preparations for CATL’s second phase were suspended indefinitely, and in the current economic climate, other investments, particularly in the automotive sector, may also be delayed.

According to GKI’s business survey, most operating companies have not even carried out major “maintenance” investments, let alone expansions into new markets, capacity increases, or development of new products. Respondents mostly cited replacing worn-out equipment as their primary investment objective. For Hungarian industry, this implies that any future upswing may be hard to exploit; dynamic growth is unlikely in the near term. Some cushion exists, however: average capacity utilisation last approached the 80% threshold in the summer of 2022 and has remained below that since. The question is how much of this underused capacity can be mobilised — and how quickly.

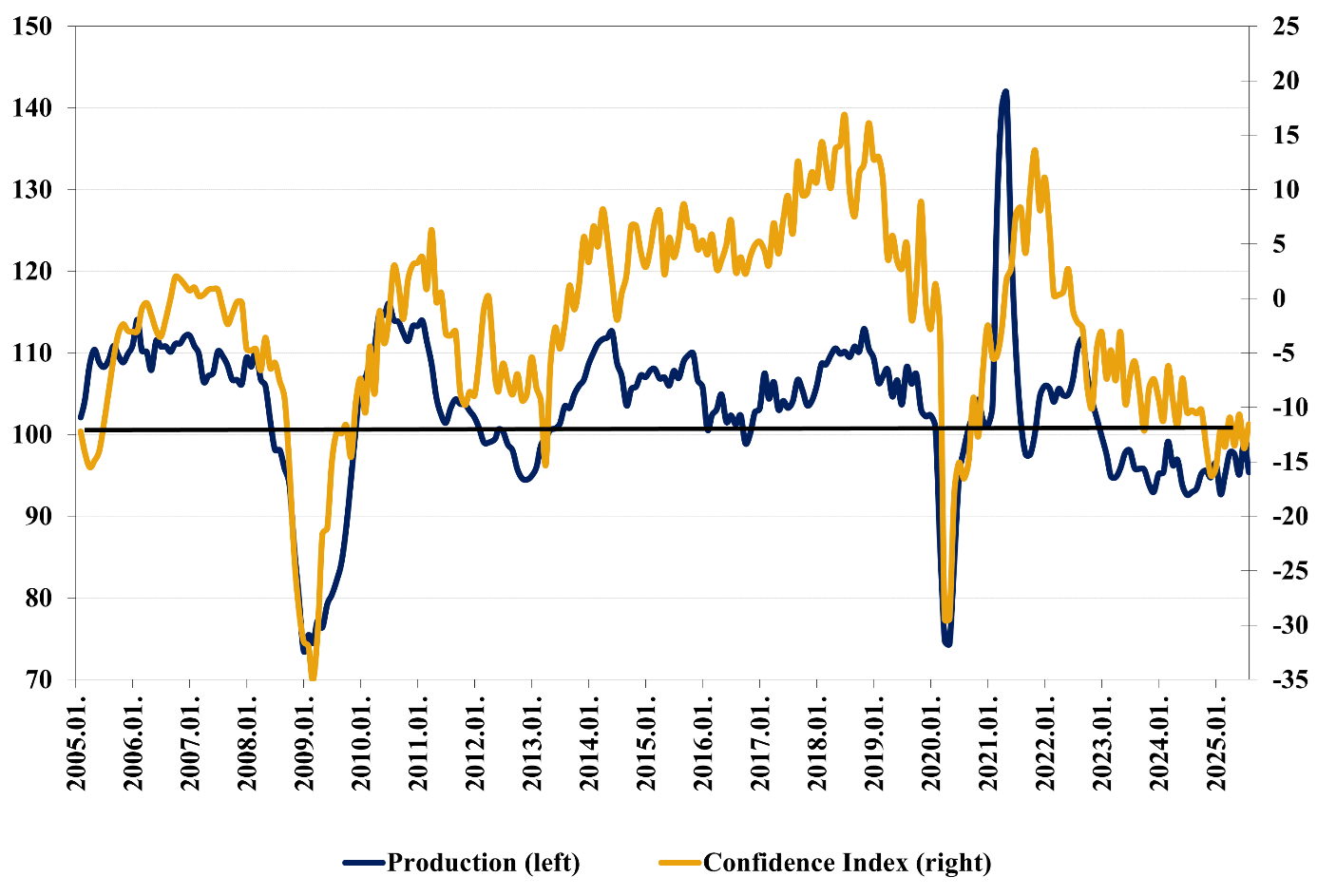

Manufacturing Output (Year-on-Year = 100) and the Industrial Confidence Index

Source: HCSO, GKI surveys

Signs of recovery are emerging in Hungary’s key markets, and prospects have improved following the US–EU tariff agreement. The rebound has begun, but progress is slow. It appears that without growth in the wider EU economy, Hungarian industry cannot return to an upward trajectory: around two-thirds of sales are exported, while domestic demand, even with artificial stimulus, is insufficient to offset weak foreign demand. New plants coming online later in the year may inject some momentum, helping to temper the decline seen in the first half. Yet based on gross production data and business confidence indicators, industrial output is unlikely to rise over the course of 2025. By the end of the year, the downturn may stabilise, and sustained growth could begin in 2026, supported by improving export prospects.

[3] GKI Estimate