Under the Otthon Start Program launched in September 2025, the preferential 3% mortgage is expected by the government to help first-time homebuyers. The conditions for the supported loan include a minimum 10% down payment, as well as a maximum DTI (debt-to-income ratio) of 50% for net incomes up to HUF 600,000, and 60% for net incomes above HUF 600,000.

From this latter limit, the maximum loan amount can be estimated, which we calculated by income deciles: we assumed the Otthon Start Program’s 3% subsidized loan up to HUF 50 million, and above that, a market-rate loan at a fixed 6.7% interest, in both cases with a 25-year term. These results were then compared with new and used apartment prices in Budapest and nationwide.

It is important to note that this gives the total amount of loan that can be taken, but it does not include the down payment. The latter depends on the individual savings of the borrower, which can be a significant obstacle for many. Furthermore, the following maximum loan amounts assume that there are no other loans – if there are, the DTI limit will further reduce the amount that can be borrowed.

Average income by decile and remaining disposable income at maximum DTI utilization

(2025, thousand HUF)

| K1 | K2 | K3 | K4 | K5 | K6 | K7 | K8 | K9 | K10 |

| 247 | 350 | 387 | 455 | 528 | 608 | 697 | 817 | 1025 | 1998 |

| 123 | 175 | 193 | 228 | 264 | 365 | 418 | 490 | 615 | 1199 |

Source: Portfolio: based on income deciles increased by 9%, calculations by GKI

The first income decile (K1), with the lowest income, can borrow a maximum of HUF 26 million based on their income, which also means they would still need nearly HUF 10 million as a down payment to purchase an average used apartment. Households with the lowest incomes typically do not have sufficient savings, so buying a used apartment is mainly a realistic option for them in less frequented areas. With the monthly installment corresponding to the loan amount they can take, the remaining disposable income is estimated to average HUF 123,000, which provides limited room for covering everyday expenses.

The second, third, and fourth income deciles (K2–K4) are in a somewhat more favorable position: they can borrow HUF 37, 41, and 48 million, respectively, which may already be sufficient to purchase an average used apartment. After paying the monthly installments, they are expected to have a remaining disposable income of approximately HUF 180,000–230,000.

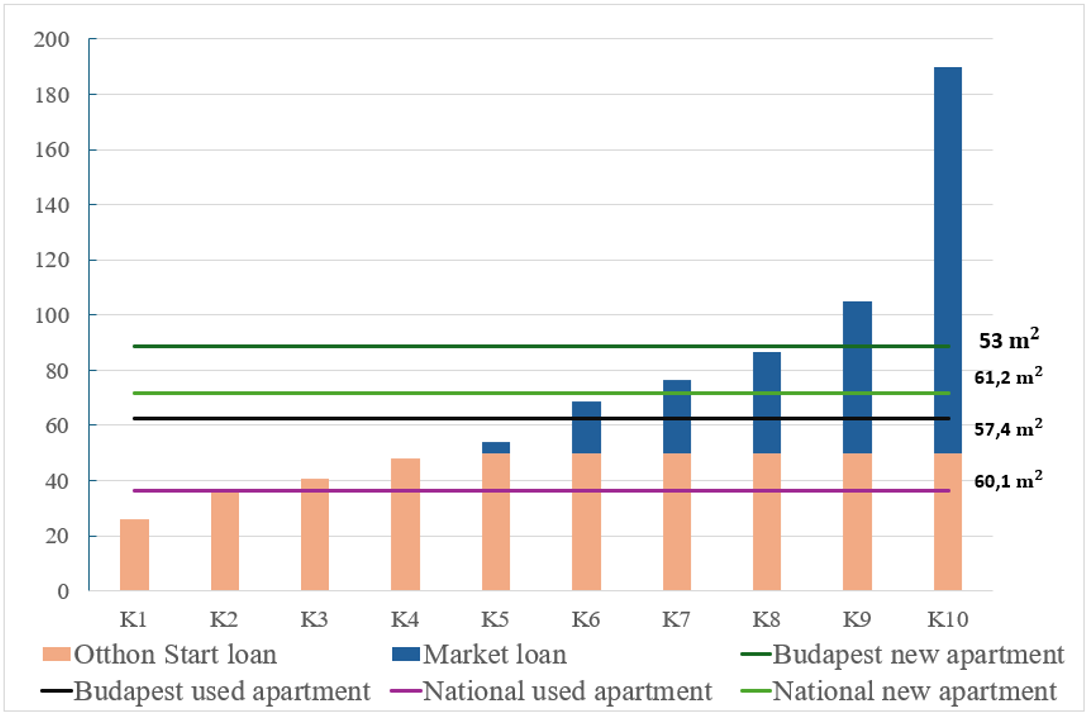

Maximum loan potential by income decile compared with average Budapest/national used/new apartment prices (million HUF)

Source: Portfolio: based on income deciles increased by 9%, KSH 2025 Q1 apartment prices, calculations by GKI

The fifth income decile (K5) is already in a more comfortable position, and with the Otthon Start Program’s maximum limit of HUF 50 million, they can also take a market-rate loan, bringing the total maximum loan amount to HUF 54 million. This allows them to find a used apartment even in Budapest with a sufficient down payment. For the sixth and seventh income deciles (K6, K7), the loan amounts they can take (HUF 69 and 77 million) are already sufficient to afford a newly built apartment in the countryside.

The eighth and ninth income deciles (K8, K9) can take on a particularly large amount of loan (HUF 86.8 and 105 million), making a new apartment in Budapest attainable, provided it meets the Otthon Start conditions. The tenth income decile (K10) has a maximum loan limit of HUF 190 million; however, the Otthon Start Program’s subsidized loan does not apply to apartments over HUF 100 million or single-family houses exceeding HUF 150 million, so all properties below these thresholds are accessible to them.

The calculations are based on the maximum debt-to-income ratio (DTI) set by the MNB, which regulates what portion of income can be used for loan repayments. However, in practice, banks may apply stricter conditions, especially for lower-income households – meaning that the actual loan amounts that can be obtained for some groups may be lower than those estimated by the model.

In summary, the Otthon Start program can provide significant support for homebuyers with medium and higher incomes. In lower-income categories, the opportunities offered by the program are likely to be truly accessible mainly for lower-priced properties in villages and small towns. The introduction of the subsidized loan stimulates demand in the short term, which may contribute to rising housing prices, especially for properties falling within the supported category. However, it is important to note that if demand in certain segments of the housing market—such as market-based purchases—declines, their real prices may also fall. For these reasons, in the long term, it is advisable to implement housing policy tools that not only support purchasing but also ensure market stability and consider the differing possibilities of various income groups.