Construction production, measured at constant prices – after two years of decline – was able to expand by 2.8% in 2025. The sectoral contract backlog at the end of December last year was almost 50% higher than a year earlier. According to the GKI survey in February, a third of the construction companies surveyed expect their sales to increase in 2026 compared to the previous year, while 21% expect a decrease. Companies with fewer than 10 employees are less optimistic in this regard, but those employing more than 50 people are much more so. Another positive sign is that the GKI sectoral confidence index rose to a thirteen-month high in February. In 2026, the volume of construction production may increase by 2-3% compared to the previous year – both domestic and international analysts agree on this.

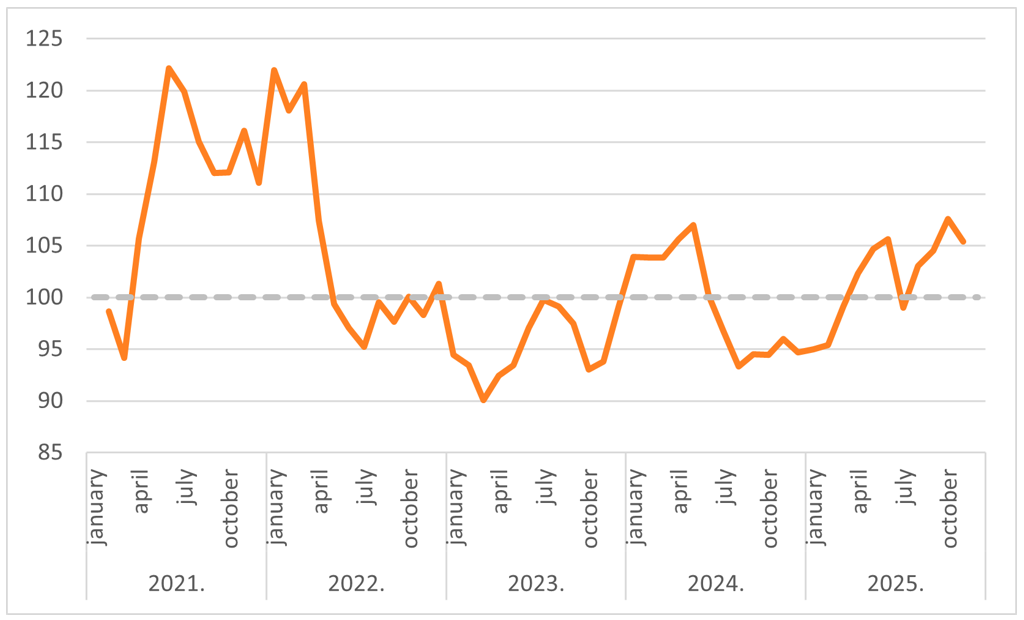

The years 2023-2024 were a difficult period for the domestic construction industry: both years brought a decline. The turbulent development of building material prices, soaring inflation and the difficulty of financing (due to rising interest rates) presented the construction industry with many challenges. Demand for construction decreased due to rising energy prices and inflation. Due to high interest rates, housing market demand and corporate investment activity declined. The decrease in EU subsidies also had a negative impact on the sector. While previously the lack of labor was the most important problem in the sector, in this period the lack of demand became the most important problem.

Last year started off difficult, but ultimately brought substantial growth

The first quarter brought a clear decline, but from April to December the sector was able to record growth in almost every month. Thus, the production volume for the whole year expanded by 2.8% compared to 2024, meaning that the growth cycle in the construction industry has started. This is necessary, because the performance in 2025 was still 4% lower than in 2022. There was a continuous decline in the stock of new contracts concluded in the first seven months of last year, and a positive change only occurred after that. At the end of December 2025, the total contract stock of the sector was almost 50% higher than a year earlier. This is fundamentally a positive sign, but it is questionable which year the multi-year contracts concluded will significantly increase the sector’s production.

Volume index of construction production, 2021-2025 (same period of previous year=100%, 3-month moving average)

Source: HCSO, GKI

Optimists are in the majority among companies regarding 2026

400 construction companies participated in the GKI survey in February 2026. 33% of those surveyed expect their sales revenue to increase in 2026 compared to 2025. At the same time, 21% fear that sales revenue may decrease on an annual basis. This means that optimists are in a slight majority compared to pessimists. Optimism also increases as company size increases. The least optimistic are companies with fewer than 10 employees, with the same two rates being 31 and 22%. In the case of companies with more than 50 employees, 55% expect revenue to increase and only 9% expect a decrease. There is nothing surprising in this: larger companies have better access to financing, their order book is more stable, and they work more often on state or large-scale projects. Companies interested in building construction are slightly more optimistic than civil engineers. In the former group, the proportion of those expecting increasing and decreasing sales is 39% and 20%, while in the latter it is 32% and 24%. Those operating in the Central Hungary region are slightly more optimistic than those working in rural areas.

Construction confidence index hits 13-month high

The confidence index, based on the results of the GKI construction survey and condensing the situation assessments and expectations of companies in the sector into a single number, reached its lowest point in June 2025. A slow but gradual increase followed. By February this year, the sector confidence index had risen to a 13-month high. This is a clearly positive development for the sector’s economy.

The start of the interest rate cut cycle could also help a lot

The construction industry is a highly credit-dependent sector, so the development of interest rates is key. The interest rate policy of the Hungarian National Bank significantly influences the financing costs of construction investments. The previous interest rate cut cycle started in 2024: after six cuts, the base rate became 6.5% and then remained there until the beginning of 2026. High bank interest rates restrained corporate credit demand between 2022 and 2025. This happened even though the government and the central bank also launched programs (such as Qualified Corporate Loan, Széchenyi Card at a fixed 3% interest rate) that aim for more favorable conditions for micro, small and medium-sized enterprises. Interest rate cuts started again at the end of February, and the central bank reduced the benchmark rate to 6.25%. Since this is likely the first step in a longer, multi-step process, it could be beneficial in the long term for financing construction companies.

According to the MNB Lending Survey, commercial banks reported a fundamentally deteriorating construction portfolio quality between 2021 and 2025, with only a slight improvement in a few quarters in the recent period. Looking ahead to 2026, banks do not expect the quality of the industry’s portfolio to become significantly more favorable. Financial institutions expect a marked increase in demand for residential real estate development in the next half of the year.

The investment market is expected to recover this year

The majority of domestic and international analysts expect investment activity in Hungary to pick up in 2026 compared to 2025. According to the GKI survey, the investment activity of companies in industry and business services will increase somewhat this year. Several significant investments will be implemented or completed in 2026. Housing construction is also expected to move away from last year’s low point, although a truly significant recovery is only expected from 2027. According to GKI, the volume of investments may increase by around 2% in 2026. This may also have a beneficial effect on the market opportunities of the construction industry.