This May Determine Whether Hungary Succeeds in the Defence Industry

Hungary’s defence industry cannot yet be considered sufficiently competitive in the international defence supply market, which makes targeted, value-added specialisation necessary. In this process, the strengthening of dual-use technologies — applicable for both civilian and military purposes — can play a key role, particularly in niche segments where domestic engineering and development competencies can provide a competitive advantage. The financing environment — especially the availability of SAFE Programme funds and their strategic, state-coordinated deployment — will be decisive in determining whether Hungary’s defence industry is capable of embarking on a meaningful growth trajectory over the coming decade and of consolidating its position at the regional level.

In 2026, GKI Economic Research Co. conducted a comprehensive study on the current state of Hungary’s defence industry and the potential breakthrough opportunities facing the sector. Publicly available, systematically organised information on the current condition, competitiveness, and financing challenges of the domestic defence industry remains limited; GKI is the first institution to have conducted a comprehensive market research study in this field, drawing on both primary and secondary sources. Based on the most recent data, the sector exhibits several development trajectories and breakthrough opportunities that — given appropriate policy and financing support — could lay the foundations for a meaningful growth path.

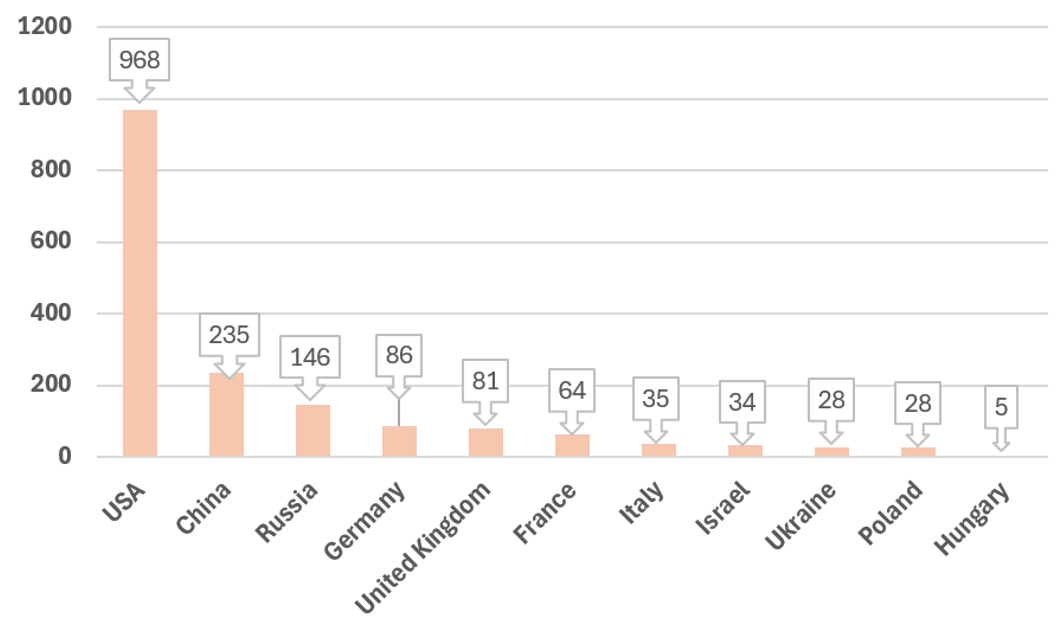

The development of the defence sector is fundamentally shaped by the transformed European security environment: since the outbreak of the Russia–Ukraine war, defence expenditures among NATO member states have been rising, and the defence industry has once again acquired strategic significance. Global defence spending reached a historic high in 2024, exceeding USD 2.46 trillion, representing a real-terms increase of 7.4% compared to the previous year. Europe’s defence expenditure also expanded dynamically: the continent’s total military spending approached USD 693 billion, reflecting an annual increase of 17% and an overall rise of approximately 83% over the past decade. In parallel, armaments investments by EU27 member states grew significantly between 2021 and 2024, rising from EUR 59 billion to over EUR 100 billion. Several EU member states rank among the world’s top defence spenders, which underscores the already considerable scale of the European defence industry.

Selected countries with high defence expenditure and Hungary’s defence spending in 2024 (USD billion)

Source: ISIS, 2025

The rapid expansion of spending is closely linked to the changed security environment, above all the Russia–Ukraine war, which has accelerated defence procurement across Europe and globally alike. A clear shift is observable in spending structures towards modern military equipment — in particular air and missile defence systems, armoured platforms, and drone technologies — while European countries are simultaneously working to expand their defence industrial capacities and reinforce their strategic autonomy.

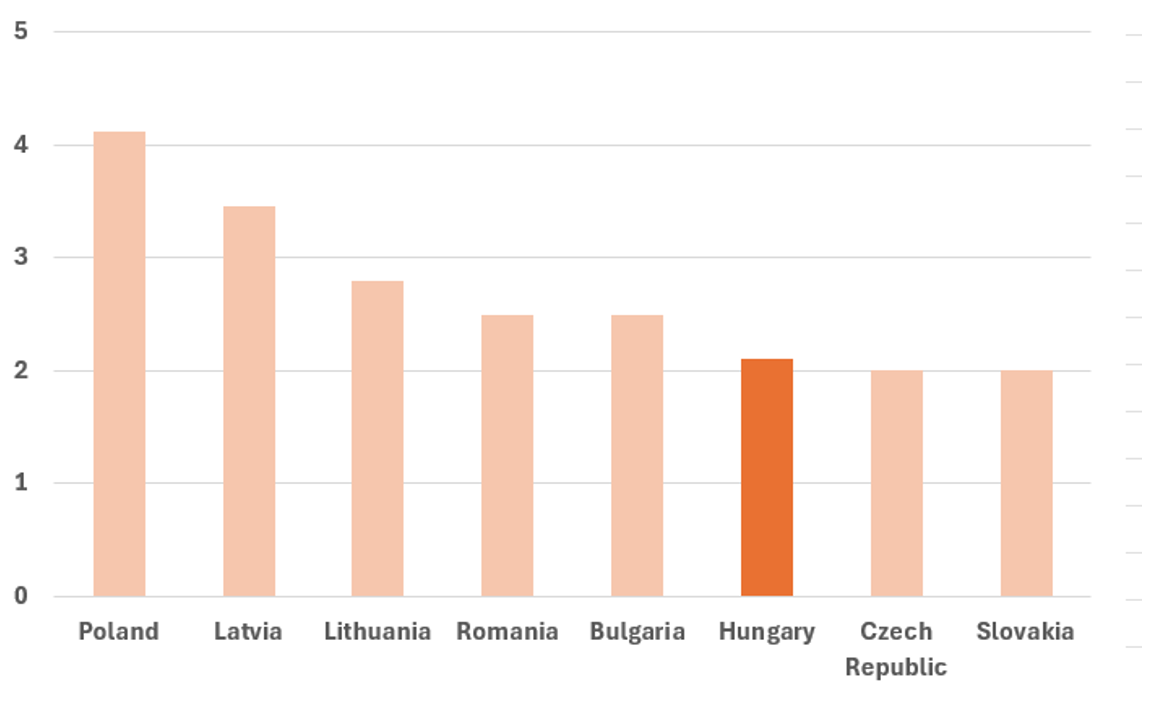

The growing international defence expenditures represent a sustained strengthening of demand, which directly benefits developments in Hungary as well. Hungary’s defence industry is simultaneously a sector that is being rebuilt and restructured. In recent years, significant capacity expansions have been initiated in armoured vehicle manufacturing, ammunition and explosives production, small arms manufacturing, and aerospace supply. As a result of successive increases in defence spending in recent years, Hungary reached and meets the NATO-required defence expenditure threshold of 2% of GDP by 2024.

Defence expenditure in Central and Eastern Europe in 2024 (as a percentage of GDP)

Source: NATO

A key characteristic of the current state of Hungary’s defence industry is that developments simultaneously serve the needs of the domestic armed forces and seek integration into international supply chains. The original objective of state-supported investments was not merely the procurement of military equipment, but also its partial domestic production, which over the longer term may yield job creation, the accumulation of technological knowledge, and export opportunities. A critical question, however, is the extent to which production represents genuine value added, as opposed to mere assembly capacity.

The most important trend is the ramp-up of land-based military equipment manufacturing. In Hungary, modern facilities capable of serial production of armoured vehicles and the supply of their components have emerged in recent years. This capability is strategically significant because demand for land-based equipment in Europe is set to remain persistently high, and it is also consistent with NATO’s expectations of Hungary. A key ongoing challenge is to broaden the domestic supplier network and to establish as many component manufacturing, maintenance, and development competencies in Hungary as possible. It must be stated that Hungary’s defence industry overall cannot yet be considered sufficiently competitive in the international defence supply market. To expand defence exports, it is advisable to focus on lower-barrier-to-entry niche markets where domestic value added — particularly through engineering and development competencies — can carry greater weight.

Against this backdrop, one of the most important directions for the development of the defence industry is the strengthening of dual-use technologies — those applicable for both civilian and military purposes. This trend is particularly important for Hungary, as the transfer of civilian industrial experience and high quality standards can help enhance the competitiveness of the defence sector. Domestically, several industry and knowledge-based opportunities exist that could simultaneously serve both the civilian economy and the defence sector, including automotive and aerospace supply, precision engineering, sensor technology, and cybersecurity.

One of the most promising directions is the defence application of automotive and mechanical engineering competencies. Hungary has a traditionally strong automotive supplier base, which — with appropriate development — could be capable of producing specialised military vehicle components, drivetrain elements, armour protection components, or maintenance systems. The dual-use dimension here lies in the fact that the same precision manufacturing processes are equally valuable in both civilian and military markets. The defence-sector utilisation of automotive capacities has become particularly timely, as the current downturn in European automotive production is accompanied by a softening of supplier demand. Consequently, identifying new, stable markets and application areas is becoming increasingly important for the supplier sector, in which the defence industry represents a potential alternative.

Significant potential also lies in the aerospace and drone technology segment. Aerospace supply requires a high culture of quality assurance and certification, which over the long term also raises the technological standards of Hungarian industry. Drones and unmanned systems represent a particularly fast-growing market: alongside agricultural, logistical, and industrial applications, military surveillance, reconnaissance, and border protection are increasingly reliant on these platforms. Hungary can become a strong player in this area if it builds capabilities not only in assembly, but also in software guidance, sensor technology, and systems integration.

The third key dual-use area is the field of cybersecurity and digital defence technologies. In modern warfare, the protection of network systems, cyber defence of critical infrastructure, and data security are of equal importance to conventional weapons systems. Hungary’s IT and engineering workforce provides a favourable foundation for cybersecurity developments to be competitive not only in the civilian economy but also in the defence sector. This will, however, require a strong research and development base, alignment with international standards, and the establishment of trusted (classified) systems.

A further important opportunity lies in the development of sensor technology, electronics, and communications systems. Radars, optical devices, navigation systems, and encrypted communications solutions are all areas that can be utilised for both civilian purposes (industrial automation, transportation, telecommunications) and military applications. For Hungary, the task here is to create higher-value-added products by linking the electronics industry with research institute capacities, and to deliberately strengthen the further development of existing corporate achievements.

For these dual-use segments to become genuine Hungarian strengths, several conditions must be met. First and foremost, there is a need for a stable and predictable industrial strategy that not only attracts investment but also defines long-term development directions for the dual-use segment. Equally critical is the development of the workforce and knowledge base: without engineering education, quality dual-track vocational training, and research and development programmes, it is impossible to build a sustainably competitive industry. To strengthen the defence industrial competitiveness of Hungarian companies — both domestically and in international markets — it is essential to establish targeted financing structures that support the sector’s specific investment and operational needs. If all of these are achieved, dual-use technologies can become one of the most stable and innovative pillars of Hungary’s defence industry.

A potentially decisive factor in terms of the financing environment is the European Union’s SAFE loan programme, to which Hungary is seeking access in order to support defence industrial investment and capacity expansion. Should the new government succeed in drawing down the loan, the SAFE programme could make a material contribution to improving the financing environment for the domestic defence industry — including in dual-use development areas such as railway infrastructure, multimodal freight terminals, and the development of logistics networks. These investments can improve not only military mobility and supply chain efficiency but also contribute directly and indirectly to Hungary’s economic growth and the strengthening of competitiveness. SAFE funds could also be complemented by European Investment Bank financing programmes, which provide additional opportunities to accelerate strategically important infrastructure development.

Based on international experience, the financing of defence and related industries is increasingly multi-sourced: alongside state and EU funds, off-budget structures are emerging, and commercial banks are also showing growing openness towards the sector. Nevertheless, it is essential that the strategic direction of available grants and credit programmes remain under state control, thereby ensuring unified, long-term development directions and guaranteeing that investments are implemented in accordance with the actual needs of the Hungarian Defence Forces and the domestic defence industry.

The most important challenge facing Hungary’s defence industry is thus the exploitation of opportunities in the dual-use segment, technological deepening, the development of the supplier network, workforce training, and the strengthening of access to international markets. If these conditions are met, over the coming decade, Hungary could become not merely a consumer but also a partial shaper of the Central European defence industrial landscape.