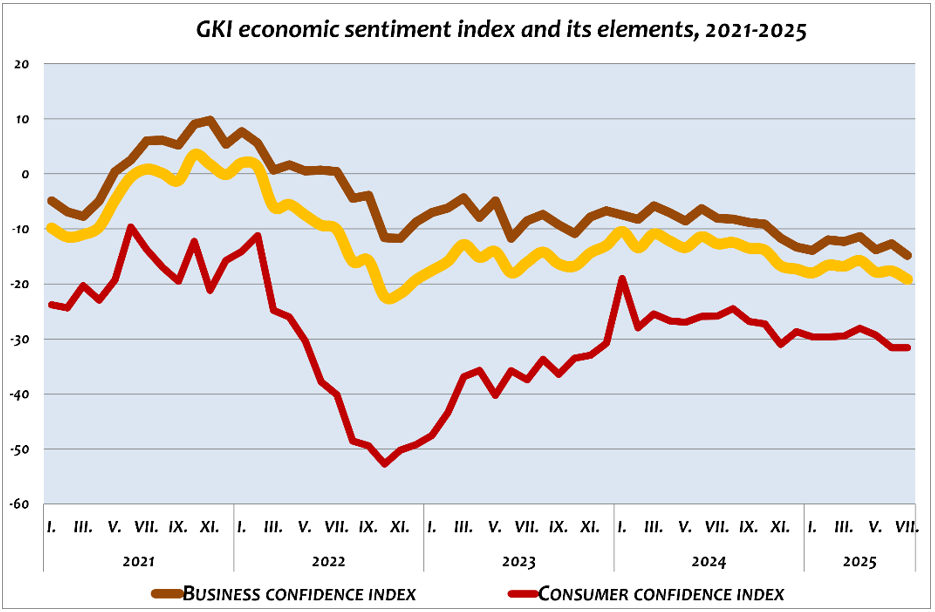

According to a survey conducted by GKI Economic Research Co. – supported by the EU – consumer sentiment in Hungary remained flat in July, while business confidence took a modest hit. As a result, the GKI economic sentiment index fell by nearly two points, sinking to its lowest level in two and a half years. Companies’ willingness to hire weakened slightly compared to the previous month. Meanwhile, a long-standing trend of declining expectations around future price increases came to a halt in July.

Following a one-point increase in June, the GKI business confidence index declined by two points in July compared to the previous survey, effectively returning to the low levels observed at the beginning of the year. The news from the services sector hardly offered any reassurance, and even less so from industry: confidence in the latter fell by three points, while in the former declined by one. Meanwhile, confidence levels in the retail and construction sectors remained unchanged. These shifts did not alter the broader picture: construction continues to be the most pessimistic sector, whereas business services remain the most optimistic.

The employment indicator, which reflects firms’ aggregated staffing intentions, declined slightly further in July. While the month-on-month change was not dramatic, the index nonetheless fell to its lowest level in nearly five years. Over the next three months, 7% of businesses plan to increase headcount, whereas 13% anticipate reducing it.

Perceptions of the predictability of the business environment deteriorated slightly in July, with the most negative assessments coming from the industrial sector.

The steady decline in the price expectations indicator, which had persisted for several months, came to a halt in July. The composite measure summarising firms’ pricing intentions only slightly but increased compared to the previous month. Encouragingly for consumers, price raising intentions in the retail sector continued to decline further. In contrast, expectations in the other three sectors saw a modest uptick. Over the next three months, 18% of firms plan to raise prices, while 8% anticipate price reductions.

The GKI consumer confidence index remained unchanged in July compared to June. Households assessed their financial situation over the past 12 months as stable, while expectations for their financial prospects over the coming year improved slightly relative to the previous month. However, perceptions of disposable income available for major purchases deteriorated modestly. Consumers viewed the country’s economic outlook for the next 12 months as slightly worse than in June — a level of pessimism not seen since September 2023. Inflation expectations among households eased, whereas outlooks regarding the future trajectory of unemployment worsened marginally.

The data presented in the charts can be found in the accompanying Excel file.

Methodological Explanation:

GKI Economic Research Co., following the methodology prescribed by the European Commission, calculates its economic sentiment index by integrating expectations from both the business sector and households (consumers). Specifically, the GKI economic sentiment index is a weighted average of the consumer confidence index and the business confidence index.

The GKI business confidence index itself is a weighted average of confidence indicators from four sectors: industry, retail trade, construction, and services. The employment indicator reflects the net balance of firms planning to increase or decrease their workforce over the next three months. Similarly, the price indicator measures the net difference between companies intending to raise or lower their selling prices within the same period.

The GKI consumer confidence index is computed as the arithmetic mean of balance indicators derived from survey responses regarding households’ assessments of their financial situation over the past twelve months, their financial outlook for the next twelve months, expectations for the country’s economic performance, and intentions to purchase durable goods.

GKI publishes seasonally adjusted data, employing appropriate mathematical techniques to eliminate distortions caused by seasonal factors – such as heightened demand before Christmas or reduced production during summer holidays.

Download full study