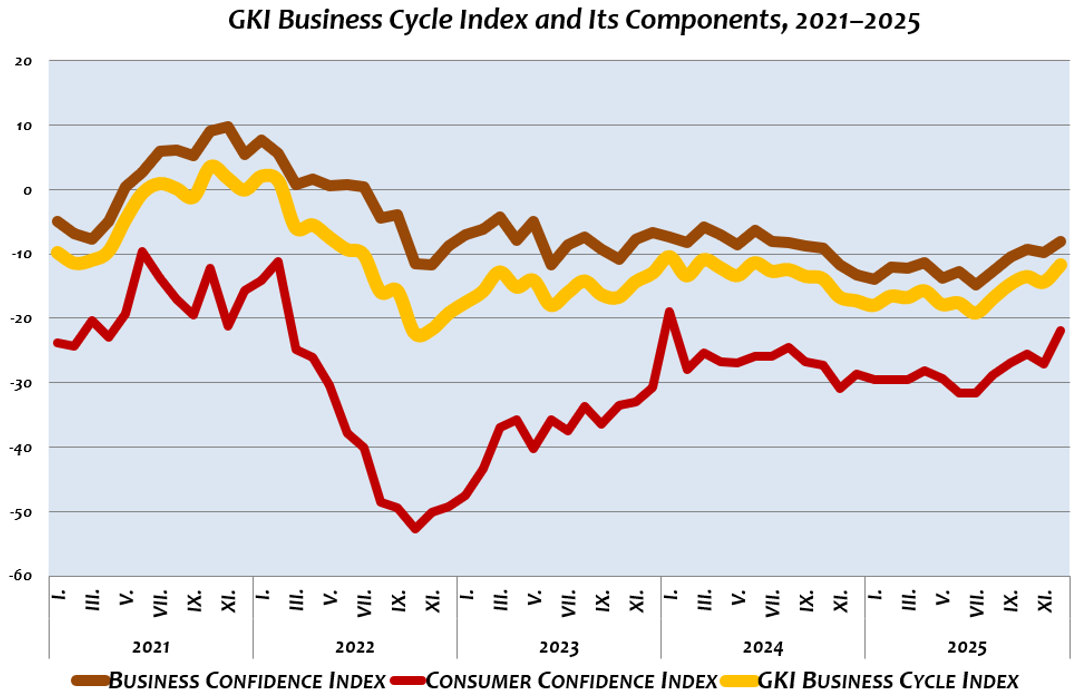

According to the survey conducted by GKI Economic Research Co. Ltd. with the support of the EU, in December the outlook of the business sector and consumers improved significantly compared to November. The summary indicator of expectations, the GKI business cycle index, rose by nearly 3 points to an eighteen-month high. At the same time, companies’ willingness to hire deteriorated slightly, while the aggregate expectation regarding the future development of selling prices stagnated compared to the previous month. In the first winter month, responding companies assessed the predictability of the business environment as having slightly worsened.

The GKI business confidence index – after the November setback – rose by 2 points in December compared to the previous month. This also represents an eighteen-month high. In this month, the industrial confidence index increased significantly, by nearly 4 points, while the commercial and services indices practically did not change, and the construction indicator fell by nearly 4 points. The industrial index was last this high twenty-one months ago. Regarding short-term prospects, construction remains the least optimistic sector, while business services is the most optimistic.

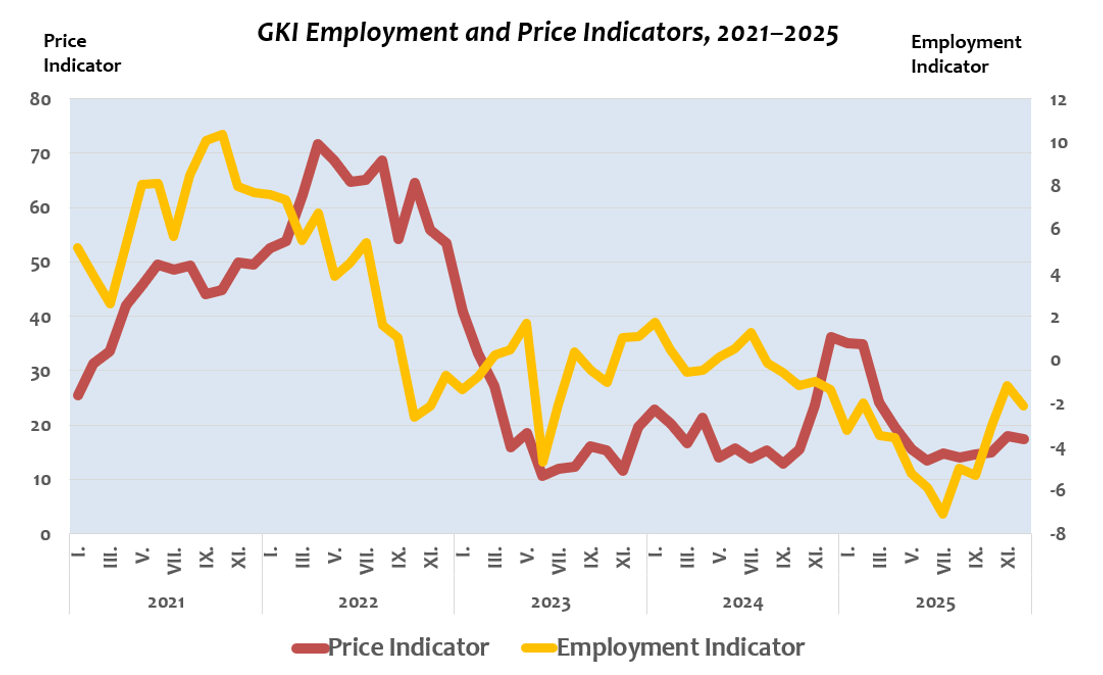

The employment indicator, which reflects businesses’ aggregate expectations regarding workforce management, declined slightly compared to the previous survey after two months of increase. Over the next three months, 8% of businesses plan to expand their workforce, while 13% intend to reduce it. In industry and in the field of business services, those seeking to expand headcount are in the majority compared to those preparing for layoffs.

The predictability of the business environment deteriorated slightly in December compared to the previous survey. Industrial and construction companies continue to suffer the most from the lack of predictability, while trading and service companies are less affected by it.

The price indicator, which shows the expected development of companies’ selling prices over the next three months, rose slightly in November compared to the previous survey after three months of stagnation, and then changed very little in December. Over the next three months, 29% of companies plan to raise prices, while 9% intend to lower them.

The GKI consumer confidence index rose significantly by 5 points in December compared to the previous survey, reaching a two-year high. All sub-indices showed noticeable improvement: the assessment of the financial situation over the past 12 months improved, as did financial expectations for the next 12 months, the evaluation of the country’s expected economic situation over the next year, and the perception of personal funds available for spending on high-value consumer goods. Household inflation expectations decreased significantly, as did expectations regarding the future development of unemployment.

The data for the charts can be found in the attached Excel file.

METHODOLOGICAL EXPLANATION:

When calculating its business cycle index – in accordance with the methodology of the European Commission – GKI Economic Research Co. Ltd. takes into account the expectations of the business sector and households (i.e., consumers): the GKI business cycle index is the weighted average of the consumer confidence index and the business confidence index.

The GKI business confidence index is the weighted average of the industrial, commercial, construction, and services confidence indices. The employment indicator reflects the difference between the proportion of companies planning to increase and those planning to reduce their number of employees over the next three months. The price indicator reflects the difference between the proportion of companies planning to raise and those planning to lower their selling prices over the next three months.

The GKI consumer confidence index is the arithmetic average of the balance indicators calculated from responses to questions regarding households’ assessment of their financial situation over the past 12 months, financial expectations for the next 12 months, anticipated developments in the country’s economic situation, and prospects for purchasing durable consumer goods.

GKI publishes seasonally adjusted data, meaning that it uses appropriate mathematical methods to filter out deviations caused by seasonal effects – for example, higher demand before Christmas or lower production due to summer holidays.

Download full study