In early 2026 Hungary issued €3 billion in euro-denominated bonds, drawing investor demand in excess of €10 billion The seven-year tranche was priced at a yield of 4.25%, while the 12-year bond carried a yield of 4.875%.

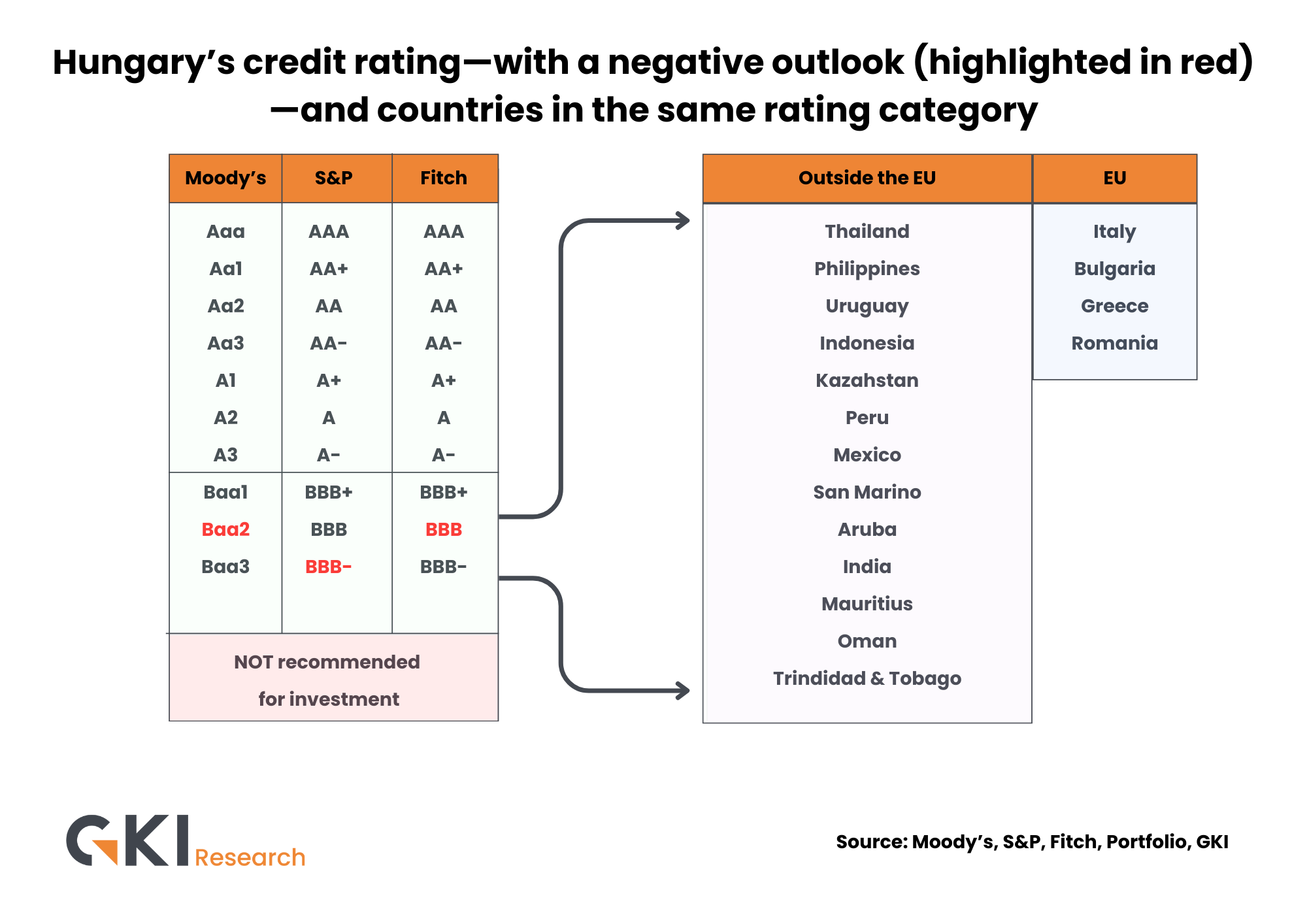

The cost of financing public debt is shaped by a combination of factors, among which the country’s risk premium plays a central role. International credit-rating agencies – Moody’s, Fitch and S&P – assess sovereign borrowers on the basis of a comprehensive evaluation of their capacity and willingness to repay, providing investors with important information about a country’s perceived risk.

Hungary is currently rated by all three agencies within the investment-grade category. At two of them, the rating sits close to the lower end of that band and carries a negative outlook; at the third, it stands one notch above non-investment grade, likewise with a negative outlook.

Based on its credit rating, Hungary is placed in the same category as countries such as Kazakhstan, the Philippines, and India. Within the European Union, only Italy, Greece, Romania, and Bulgaria share this band, while all other member states hold more favourable ratings.

Bond-market yields reflect this assessment of risk. Yields on long-dated, forint-denominated government bonds rank among the highest in the European Union. Yields on Hungarian euro-denominated bonds also exceed the averages of regional peers with similar ratings (Italy: ~3.45%, Greece: ~3.37%, Romania: ~3.9%, Bulgaria: ~3.1%, Hungary: ~4.2–4.9%). An improvement in the rating could reduce the country risk premium, potentially lowering financing costs over the longer term.

Criteria used by credit-rating agencies

Credit-rating agencies consider multiple factors when assessing a country’s sovereign rating. These include the economy’s growth prospects, the budget balance and the sustainability of public debt, as well as the country’s external vulnerabilities. Equally important are the predictability of economic policy, the functioning of institutional frameworks, political stability, the credibility of central-bank policy, and the environment for exchange rates and inflation. Access to EU funds is also regularly reflected in their assessments. Beyond these, growth prospects, external balance, and longer-term structural factors – such as demographic trends, productivity developments, and the state of human services – play a key role.

Fiscal outlook

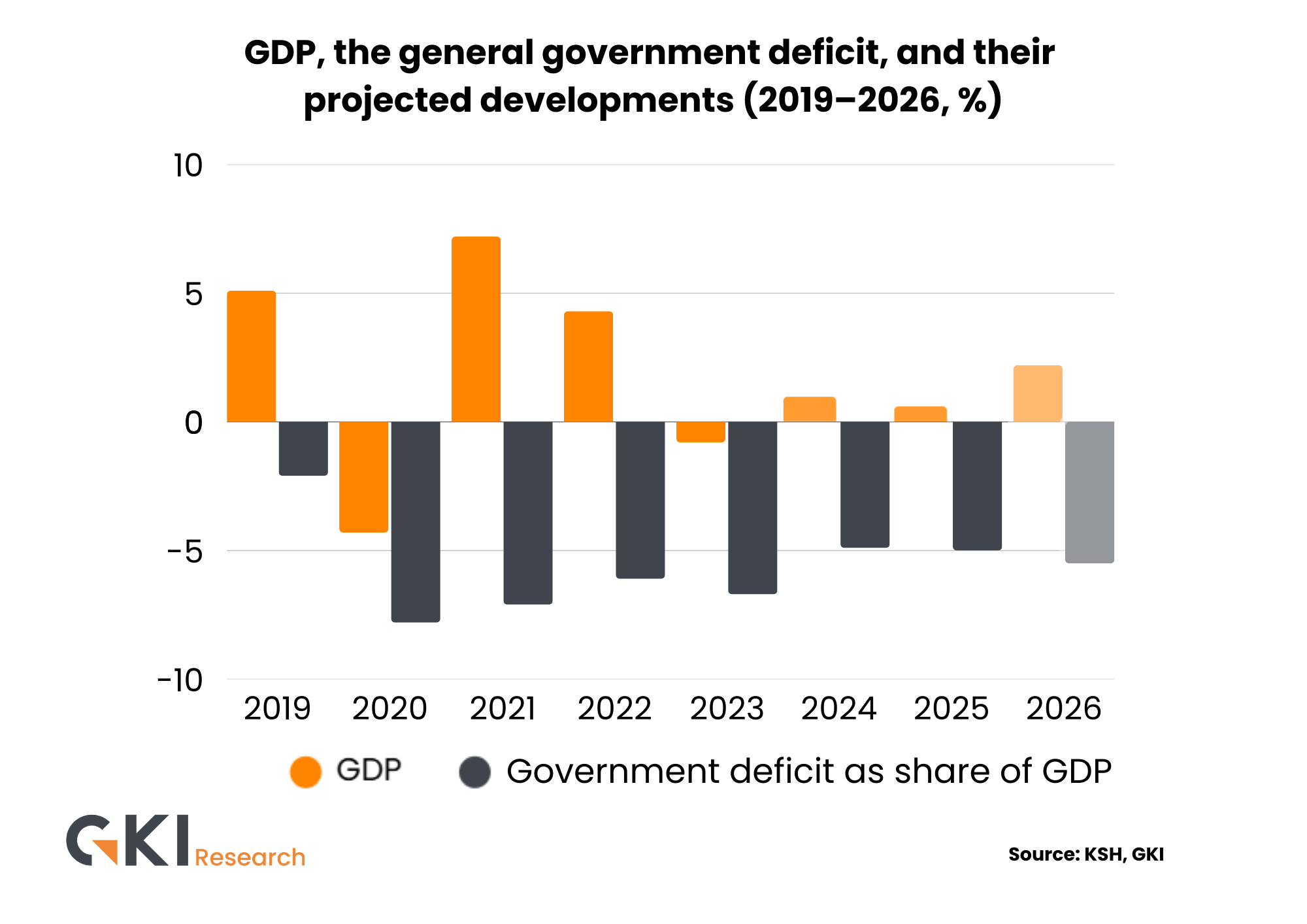

Hungary’s budgetary policy in 2025 faced a narrowing fiscal space: the deficit approached 5% of GDP, while public debt edged slightly higher.

The government currently expects the deficit to remain elevated in 2026, around 5%. The prevailing expert consensus projects domestic GDP growth at roughly 2%, compared with the government’s forecast of 3.1%. Should actual economic growth fall short of government expectations, and if high interest payments persist while corrective measures are delayed, the deficit in 2026 could exceed planned levels.

In this context, a key question is how international credit-rating agencies view the situation. The sustainability of the deficit path, the credibility of debt management, and the predictability of economic policy play a central role in shaping rating outlooks. Understanding the link between fiscal balance and credit ratings is important, as it highlights the main priorities and the risks of downgrade.