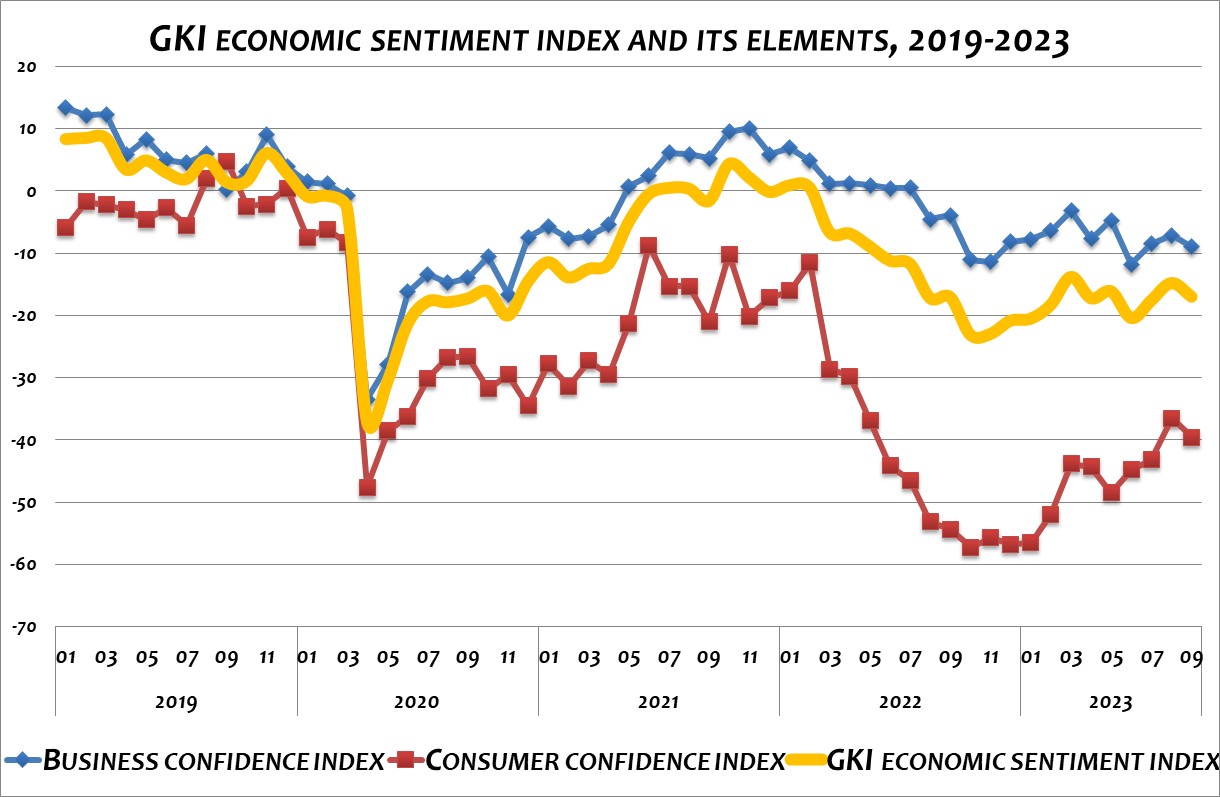

With the arrival of autumn, households and businesses also became a little more pessimistic. According to the empirical survey conducted by GKI Economic Research Co. with the support of the EU, consumer and business expectations also deteriorated somewhat in September, with GKI’s economic sentiment index falling by a narrow 2 points compared to August. In the first autumn month, the relatively favourable employment expectations of companies did not change significantly compared to August; however, their intentions to raise prices increased slightly.

After rising for two months, the GKI business confidence index declined modestly in September. In the first autumn month, the sectoral outlook worsened in industry and construction, while it remained unchanged in trade and services. Among the factors that make up the confidence index in industry, the assessment of self-produced inventories practically did not change, the expected production in the next 3 months deteriorated to a lesser extent, and the assessment of the entire stock of orders deteriorated to a greater extent compared to August. In construction, the assessment of the stock of orders deteriorated significantly, whereas employment expectations only deteriorated within the statistical margin of error. In trade, the assessment of the level of inventories deteriorated significantly, the assessment of the business performance of the previous 3 months improved slightly, and the assessment of orders expected in the next 3 months hardly changed. In services, business sentiment improved slightly over the previous three months and turnover expectations improved slightly more markedly compared with August.

Households’ mood improved steadily in the summer months, but the arrival of autumn brought some slowdown: the GKI consumer confidence index fell by 3 points in September, from a record 16-month high in August. In the ninth month, all four of the sub-indicators that make up the consumer confidence index worsened. Households assessed their own financial situation in the past 12 months as worsening compared to the previous month, and had a similar view for the next 12 months. Households’ perception of their ability to spend money on high-value consumer goods over the next 12 months also deteriorated slightly.

Businesses’ propensity to hire remained unchanged in September, with the same prospect of redundancies and staff increases. Pessimists were in the majority in construction, while optimists were in the majority in trade and services. In industry, these two ratios were the same. Fear of unemployment eased slightly among households.

In September, the intentions of the business sector to raise prices strengthened slightly, while the inflationary expectations of consumers eased slightly compared with August. Households and businesses also had a slightly different view of the future prospects for the Hungarian economy, with the former’s view deteriorating slightly and the latter’s improving markedly.

Explanation to the methodology:

In line with the methodology used by the European Commission, GKI surveys the expectations of industry, trade, construction, services (the latter, as in the EU, excludes financial and public services) and households in the calculation of its business confidence index. GKI’s economic sentiment index is the weighted average of the consumer confidence index and the business confidence index.

The business confidence index is the weighted average of the industrial, trade, construction and services confidence indices. The industrial confidence index is derived from the responses to questions on business perceptions of incoming orders and inventories, and on production expectations. The construction confidence index is the average of the perception of incoming orders and employment expectations. The trade confidence index is the average of business and inventory level perceptions and turnover expectations. The services confidence index is the average of business confidence, turnover and employment expectations. GKI publishes seasonally adjusted data by using appropriate mathematical method (the Tramo Seats method) to filter out the discrepancies caused by seasonal effects (e.g., differences in weather conditions between winter and summer, increased demand before Christmas, lower output because of summer vacations).

The consumer confidence index is compiled from responses to questions concerning the past and expected financial position of households, the expected economic situation of the country, and the prospects for purchasing consumer durables.

Download full study