Analysis by GKI Economic Research suggests that while rating agencies monitored the Hungarian elections with intensified scrutinya, decisive judgment is improbable during the upcoming review cycle. Currently, Hungary’s sovereign debt is teetering near the lower boundary of the investment-grade category at all three major agencies—Fitch, Moody’s, and S&P—all of which maintain a negative outlook. The first major test arrives on May 22 with Moody’s scheduled review. However, the S&P review a week later is considered the critical flashpoint: Hungary sits a mere notch above speculative (junk) grade in their books.

While rating agencies reserve the right to take ad-hoc action, an immediate downgrade before the new government is fully seated remains unlikely. Recent communications suggest these institutions are waiting for a clear fiscal stabilization roadmap. Consequently, there is a high probability they will maintain current ratings for now, deferring a substantive reassessment until the second review cycle this autumn, pending the unveiling of the new administration’s economic policy.

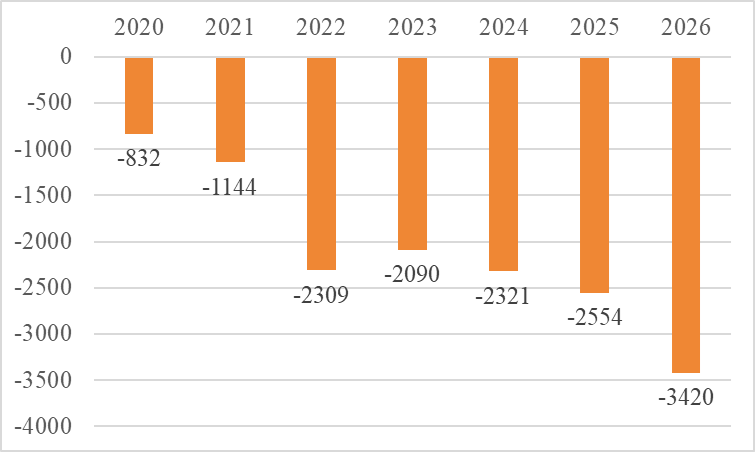

Central Government Budget Deficit to the end of March (Billion HUF, 2020–2025)

Source: Ministry for National Economy (NGM)

Regional precedents offer some solace; neither the 2021 political pivot in the Czech Republic nor the 2023 shift in Poland triggered immediate rating revisions. Domestically, however, drafting a new budget is a matter of urgency. By the end of March, the fiscal deficit had already breached 80% of the original full-year statutory target. Even when measured against the government’s revised 5 trillion HUF target, the first quarter’s 3.4 trillion HUF shortfall represents 68% of the annual limit.

The new administration inherits a rigid spending structure. A significant portion of the early-year outlays consists of long-term, politically sensitive commitments that are difficult to roll back. These include interest-subsidized credit programs (such as “Home Start” and various corporate loan schemes), PIT exemptions for mothers with three (and partially two) children, further hikes in family tax allowances, and public sector wage increases.

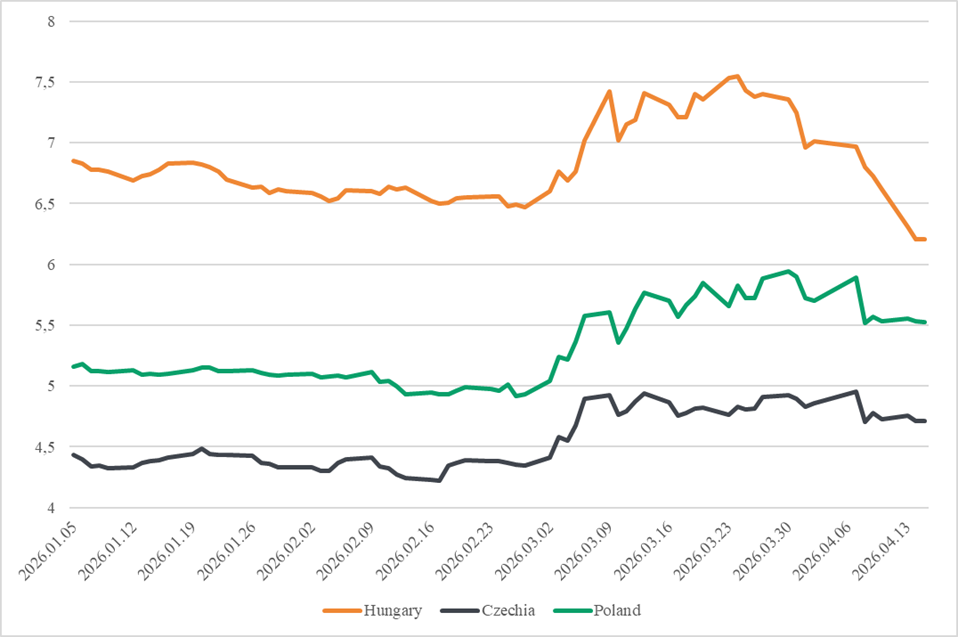

10-Year Government Bond Yields: Hungary, Poland, and Czech Republic (Percentage, Jan 2026 – April 2026)

Source: Investing.com

According to research by the Open Budget Survey, Hungary’s fiscal transparency has lagged behind its regional peers in recent years. Restoring the confidence of both investors and agencies will require a concerted effort toward budget clarity and the consistent implementation of fiscal adjustments.

The primary catalyst for a rating turnaround remains the unlocking of frozen European Union funds (Cohesion and Recovery Funds). In analyses published in the days following the election, all three major agencies emphasized that securing these funds is pivotal to bolstering Hungary’s growth outlook and external balance, thereby strengthening its creditworthiness.

Investor sentiment post-election suggests a perceived reduction in domestic fiscal risk. This is reflected in the divergence of long-term yields: while regional yields remain above their January levels, Hungarian 10-year yields have retreated nearly 150 basis points from their March peak, now trading well below their year-to-date starting point.