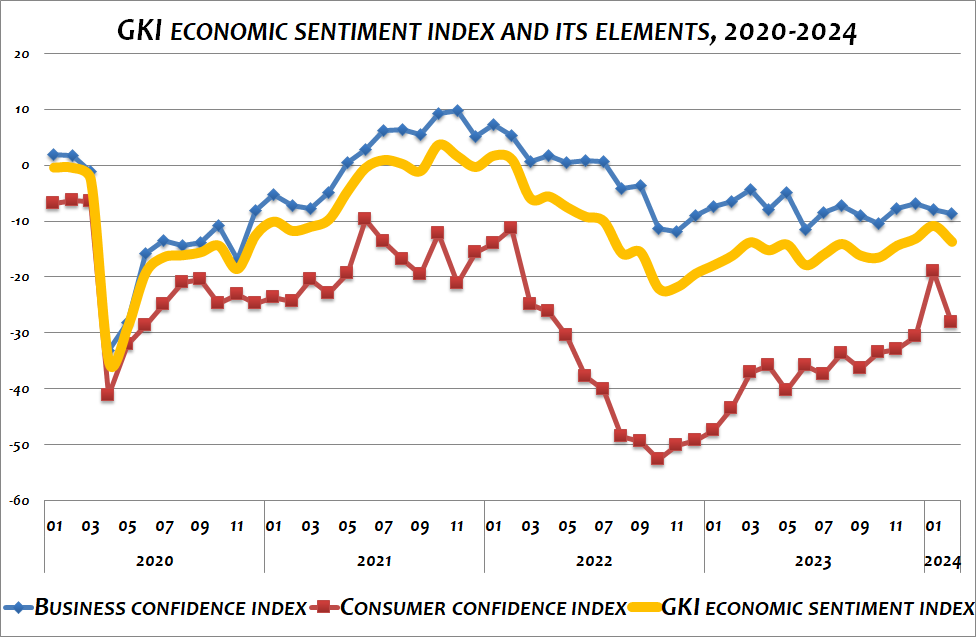

According to a survey conducted by GKI Economic Research Co. with the support of the EU, business expectations changed in February only within the statistical margin of error, but household expectations deteriorated significantly after the exceptionally positive January data. As a result, the GKI economic sentiment index fell by 3 points compared to January. The employment intentions of companies did not change significantly, while their price increase plans eased somewhat. The predictability of the business environment fell to a 13-month low.

The GKI economic sentiment index fell by 3 points in February, after a solid 2-point rise in January, essentially returning to its year-end level. Business sentiment did not improve in February either, in fact, the GKI business confidence index fell within the statistical margin of error. In February, there was a noticeable negative change in industry and construction (down 2 and 4 points, respectively), but the picture was brighter for trade and business services (up 4 and 1.5 points, respectively). In industry, the assessment of total order books reflected less satisfaction than in January, and the production outlook for the next three months also deteriorated somewhat, while the level of stocks of own production was little changed. In construction, the assessment of order books and employment expectations also changed in a negative direction. In trade, satisfaction with the previous three months’ business increased, inventories fell and the outlook for orders in the next three months also improved. In services, the assessment of the business performance of the previous three months deteriorated markedly, but turnover expectations for the next three months improved significantly compared with January, while employment plans were little changed. This was the only truly optimistic sector.

Businesses’ propensity to hire did not change significantly in February, and the proportion of those planning to expand and reduce staff numbers was not materially different. Optimists made up the majority in trade and business services, while pessimists in industry and construction. Overall price increase plans in the business sector declined slightly in February, after two months of strengthening, but they strengthened somewhat in trade and services. The predictability of the business environment became noticeably less favourable, and this indicator fell to a 13-month low.

After rising in December and January, the GKI consumer confidence index showed a strong negative correction in February. The February index, after a spike in January, was in line with a positive trend that had been in place for almost a year and a half. In February, households assessed both their financial situation in the last 12 months and their financial prospects for the next 12 months as strongly improving, and their perception of their own money to spend on high-value consumer goods was also worse than in the previous month. Respondents also saw the economic outlook for the country over the next 12 months as much less positive. However, inflationary expectations of households decreased somewhat compared to the first month of the year and they were less worried about unemployment than in January.

Explanation to the methodology:

In line with the methodology used by the European Commission, GKI surveys the expectations of industry, trade, construction, services (the latter, as in the EU, excludes financial and public services) and households (consumers) in the calculation of its business confidence index. GKI’s economic sentiment index is the weighted average of the consumer confidence index and the business confidence index.

The business confidence index is the weighted average of the industrial, trade, construction, and services confidence indices. The industrial confidence index is derived from the responses to questions on business perceptions of incoming orders and inventories, and on production expectations. The construction confidence index is the average of the perception of incoming orders and employment expectations. The trade confidence index is the average of business and inventory level perceptions and turnover expectations. The services confidence index is the average of business confidence, turnover and employment expectations.

The consumer confidence index is the arithmetic average of balance indicators calculated from responses to questions on households’ perceptions of their financial situation in the past 12 months, their financial prospects for the next 12 months, the expected development of Hungary’s economic situation and their prospects for buying consumer durables.

GKI publishes seasonally adjusted data by using appropriate mathematical method to filter out the discrepancies caused by seasonal effects (e.g., differences in weather conditions between winter and summer, increased demand before Christmas, lower output because of summer vacations). The historical data now published are different from those published previously, as seasonally adjusted data are revised once a year (in January).

Download full analysis