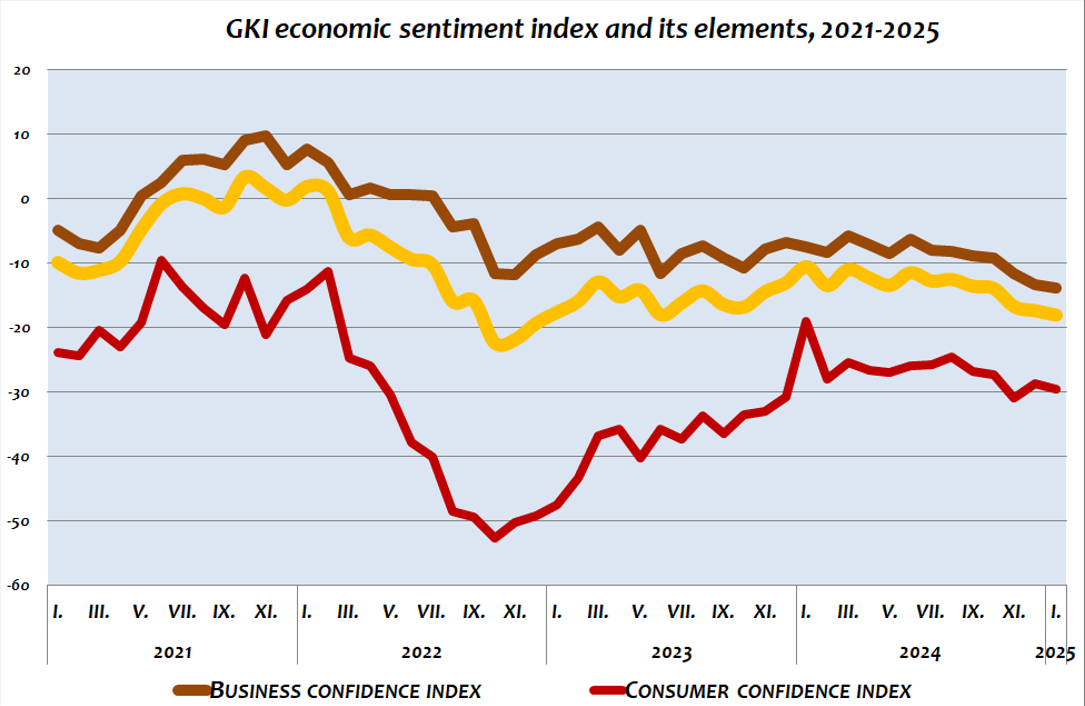

In the first month of this year, the slightly negative trend continued: according to the EU-supported GKI Economic Research Co. survey, the expectations for both the business sector and consumers worsened compared to December, although in both cases only within the statistical margin of error. Even so, the GKI economic sentiment index slipped to a 19-month low. However, the predictability of the economic environment improved slightly.

The GKI business confidence index fell within the statistical margin of error in January but still slipped to a 50-month low. The industrial and construction confidence indices rose within the margin of error compared to the previous survey. At the same time, the retail trade index was down slightly, and the business services confidence index fell sharply. Still, retail trade remains the least and business services the most optimistic sector.

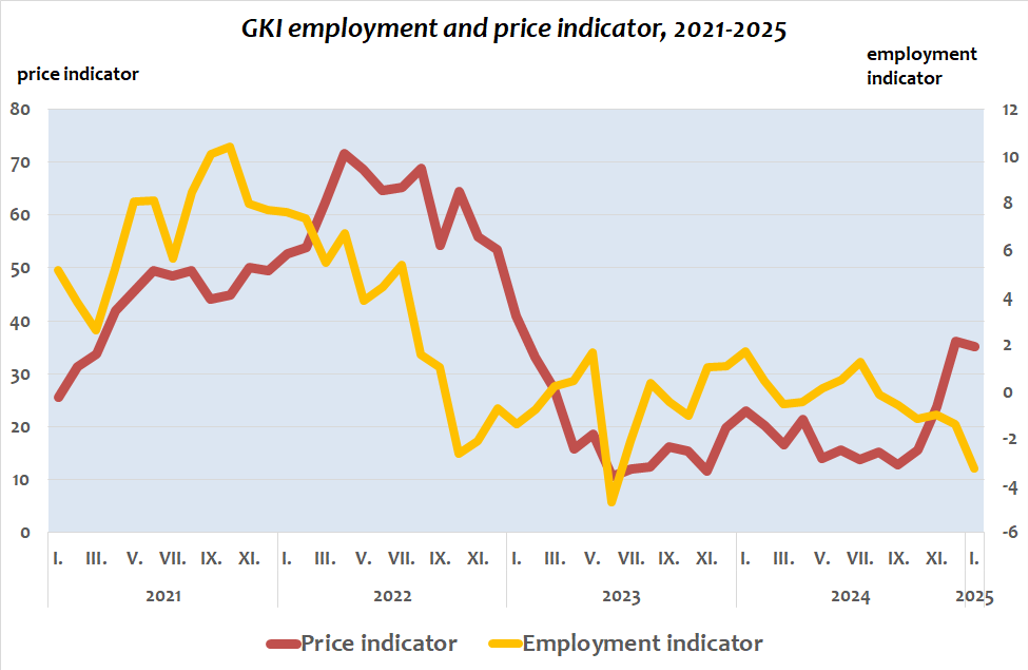

The employment indicator, which measures the aggregate employment propensity of businesses, fell slightly in January compared with December, falling to a 19-month low. Employment intentions deteriorated in industry, construction and services compared to the previous month, while the outlook for trade improved. In the next three months, 9% of businesses are planning to expand their workforce, while 14% are planning to lay off workers. After two months of deterioration, the perception of the predictability of the business environment improved markedly in January compared to December.

The price indicator, which condenses business price plans into a single figure, fell slightly in the first month of this year compared with the previous month. Only in the retail trade sector was a strengthening of price increase intentions. Half of firms plan to raise prices in the next three months, while only 5% intend to cut prices.

The GKI consumer confidence index barely changed in the March-September period, before starting to decline markedly in the autumn months last year. A positive correction in December was followed by a slight decline in January. The consumers felt that their financial situation over the past 12 months was slightly better than in the previous month. At the same time, their own financial outlook for the next 12 months and the country’s economic situation were also assessed as worsening. The perception of own money to spend on high value consumer goods remained unchanged on a monthly basis. The consumers’ inflation outlook fell slightly, while the outlook for the number of unemployed people improved slightly compared with the last month of last year.

The data for the figures can be found in the attached Excel file.

Explanation to the methodology:

In line with the methodology used by the European Commission, GKI surveys the expectations of industry, trade, construction, service sector and households (consumers) in the calculation of its business confidence index. GKI economic sentiment index is the weighted average of the consumer confidence index and the business confidence index.

The GKI business confidence index is the weighted average of the industrial, trade, construction, and services confidence indices. The employment indicator is the difference in the proportion of firms planning to increase or decrease their staff over the next three months. The price indicator is the difference in the proportion of firms planning to increase or decrease their sales prices in the next three months.

The consumer confidence index is the arithmetic average of balance indicators calculated from responses to questions on households’ perceptions of their financial situation in the past 12 months, their financial prospects for the next 12 months, the expected development of Hungary’s economic situation and their prospects for buying consumer durables.

GKI publishes seasonally adjusted data by using appropriate mathematical method to filter out the discrepancies caused by seasonal effects (e.g., ncreased demand before Christmas, lower output because of summer vacations).