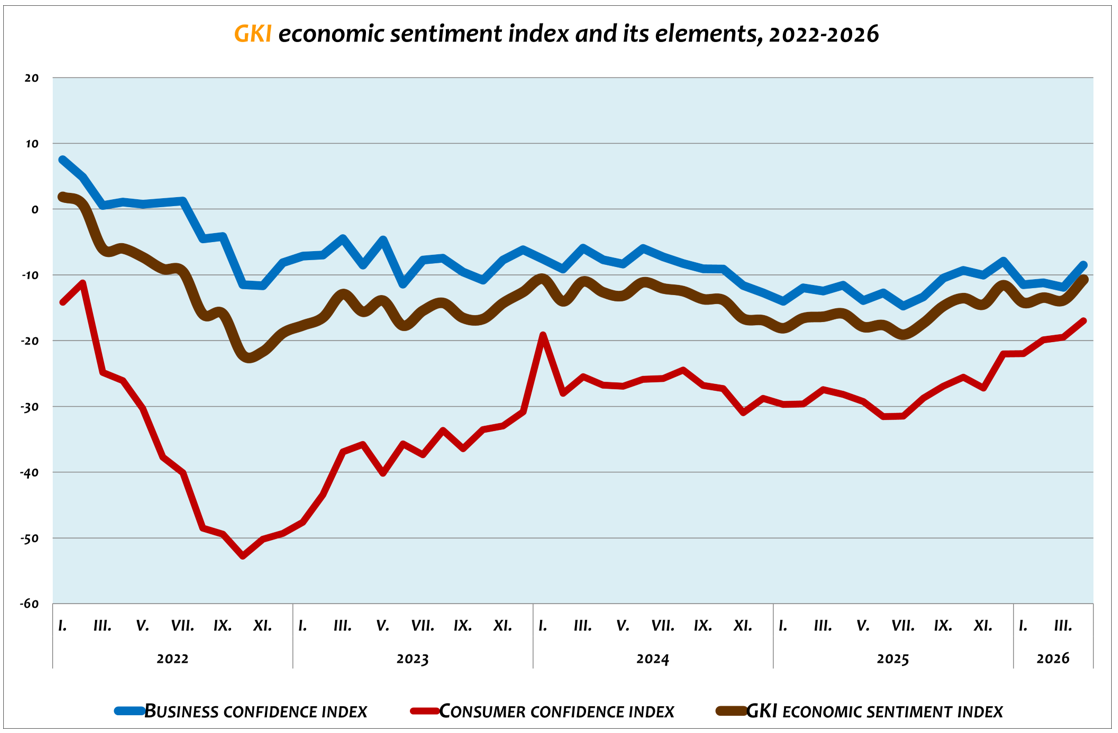

According to a survey by GKI Economic Research Ltd. – conducted with the support and methodology of the EU – the mood of consumers and the business sector improved noticeably in April compared to March. The summary indicator of expectations, the GKI economic sentiment index rose by a good three points compared to March, reaching a twenty-seven-month high. At the same time, the willingness of businesses to employ deteriorated slightly, and the outlook for the expected development of sales prices increased significantly. The responding companies felt that the business environment was somewhat more predictable in the fourth month of this year than in the previous month. The survey responses were received in the first half of April, so the impact of the parliamentary elections will be shown in the May survey.

The GKI business confidence index rose noticeably in April, by more than three points compared to the previous month, reaching a four-month high. The industrial confidence index increased by 4 points, the construction index by 5 points, and the trade index by almost 6 points. The service sector index produced a modest increase of 1 point. Regarding the prospects for the near future, the construction continues to be the least optimistic, while business services are the most optimistic sector.

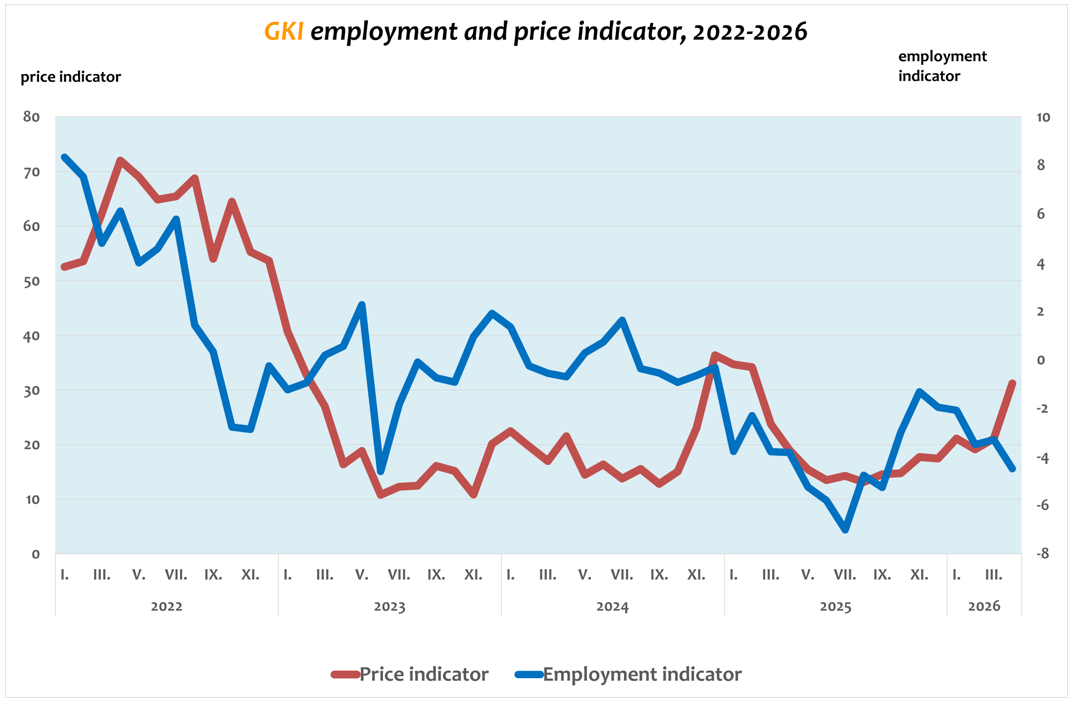

The employment indicator, which indicates the aggregated staffing expectations of enterprises, decreased slightly in the fourth month of 2026 compared to March. In the next three months, 8% of enterprises are preparing to increase their staff, while 11% would reduce it. In construction and trade, those seeking to reduce their staff are in the majority compared to those planning to expand, in industry these two proportions are practically the same, while in the services sector the latter are in the majority.

Assessing the predictability of the business environment in April improved slightly. Except for industry, respondents in all sectors felt the environment was more predictable than in March.

The price indicator, which shows the expected development of companies’ selling prices over the next three months, rose to a one-year high in April. In the next three months, 35% of companies plan to raise prices, while 5% plan to cut prices – compared to 30% and 8% in March.

The GKI consumer confidence index jumped from the range between (-25) and (-32) points typical of the past two years to (-22) points in December, and then, after stagnation in January, it gradually rose from February – by a good 3 points in April compared to the previous month. This reached a twenty-eight-month high for this indicator. The population assessed the country’s economic situation over the next 12 months as strongly improving. The assessment of the financial situation over the past 12 months and the outlook for the next 12 months deteriorated slightly compared to March. However, the assessment of the amount of money that can be spent on high-value consumer goods improved. The population’s inflation expectations barely changed, while the outlook for the expected development of the number of unemployed people deteriorated slightly.

The data for the figures can be found in the attached Excel file.

Methodological explanation:

When calculating the economic sentiment index, GKI Economic Research Co.. – in accordance with the methodology of the European Commission – takes into account the expectations of the business sector and the population (i.e. consumers): the GKI economic sentiment index is the weighted average of the consumer confidence index and the business confidence index. The GKI business confidence index is the weighted average of the industrial, commercial, construction and service confidence indices. The employment indicator is the difference between the proportion of companies planning to increase or reduce the number of employees in the next three months. The price indicator is the difference between the proportion of companies planning to increase or reduce sales prices in the next three months. The GKI consumer confidence index is the arithmetic average of the balance indicators calculated from the answers given to questions asking about the assessment of the financial situation of households in the past 12 months, the financial outlook for the next 12 months, the expected development of the country’s economic situation, and the outlook for the purchase of durable consumer goods. The GKI publishes seasonally adjusted data, meaning that it uses the appropriate mathematical method to filter out differences caused by seasonal effects – such as higher demand before Christmas, lower production due to summer holidays.

Download exclusive detailed analysis Download background data