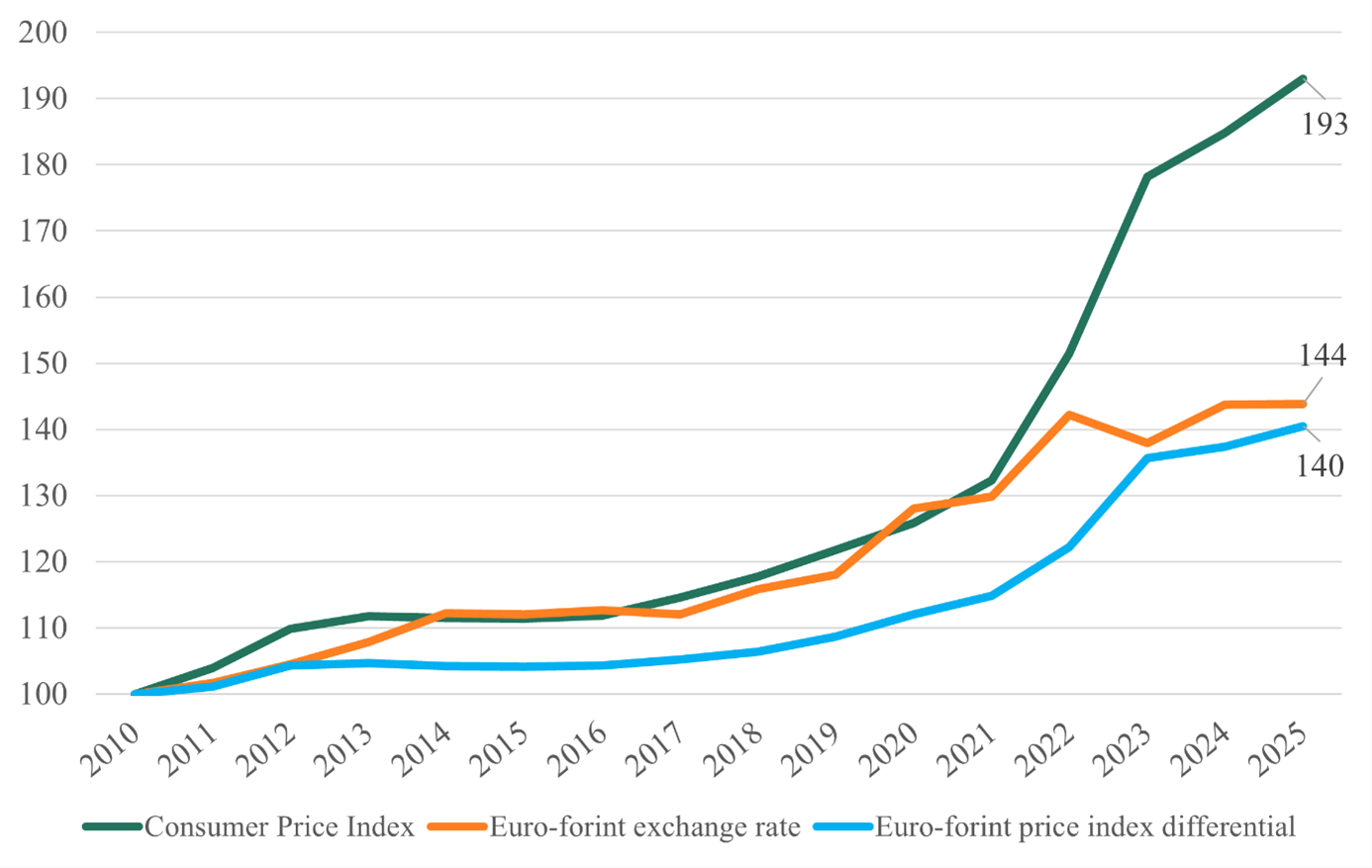

Since 2010 Hungary’s consumer price index has nearly doubled, while in the euro area prices have risen by just 38%. That disparity alone implies that, under a fixed exchange rate, the international competitiveness of Hungarian firms would have deteriorated markedly: measured in euros, their operating costs would have increased far faster than those of their foreign rivals. Yet this effect was partly offset by the forint’s gradual depreciation against the euro. Exporting firms were thus able to preserve their price competitiveness. The cost, however, was higher prices for imported goods and services.

The time series show that from 2019 onwards Hungary’s annual average consumer price index persistently exceeded the central bank’s 3% target, before reaching extreme levels in 2022 and 2023 (14.5% and 17.6%, respectively). Over the same period the gap between the Hungarian and euro-area price indices widened markedly, meaning that prices in Hungary rose far faster than in the countries of the single currency. Meanwhile the euro appreciated by roughly 45% against the forint: the annual average exchange rate, around 275 per euro in 2010, climbed to nearly 400 over the following fifteen years. This sustained depreciation contributed materially to the rise in Hungary’s domestic price level.

Consumer price index, euro–forint exchange rate

and the euro–forint price index differential 2010–2025 (2010 = 100)

Source: GKI calculations (2026), based on data from KSH, Eurostat and Investing.com.

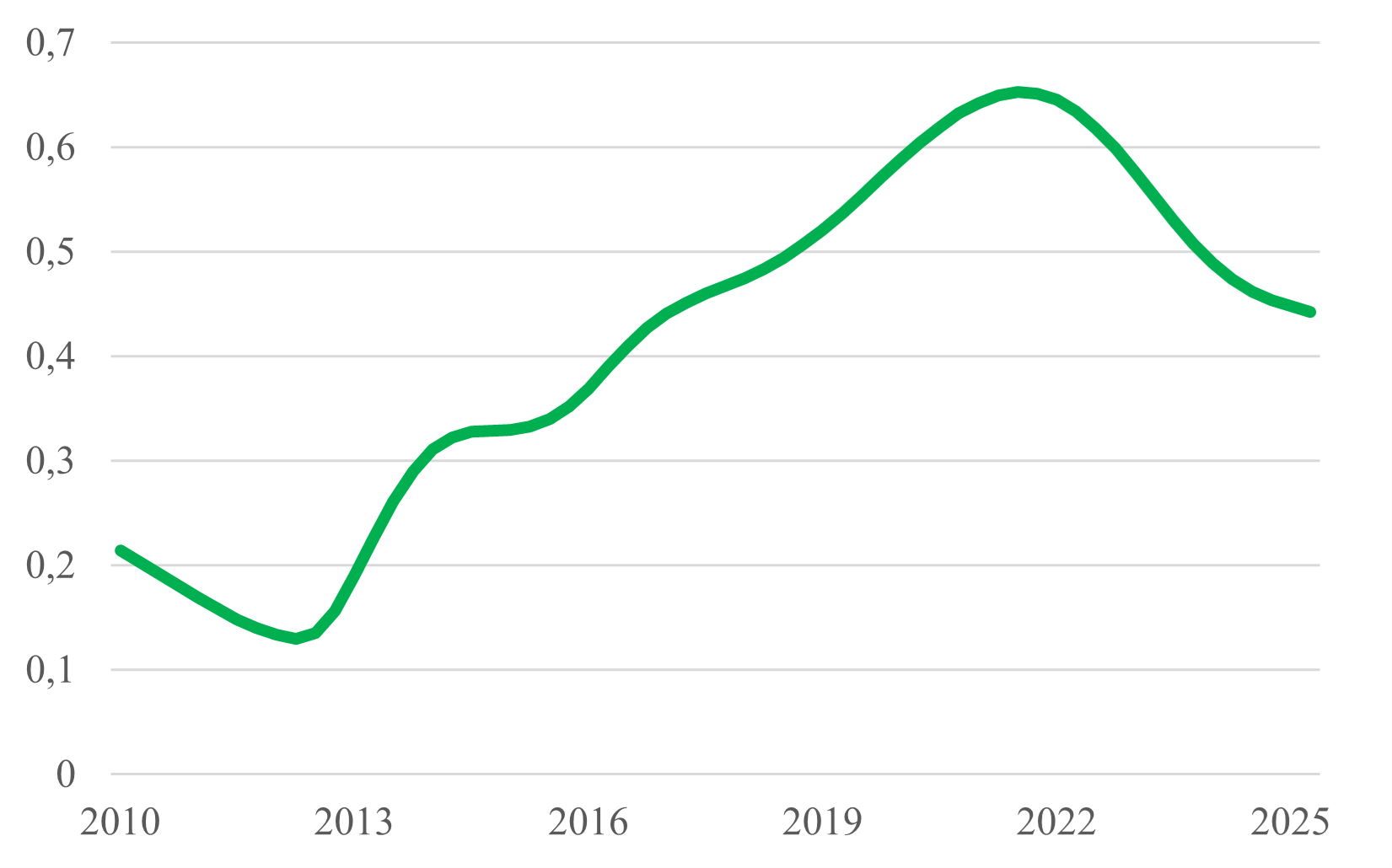

Based on its DSGE model developed for the Hungarian economy, GKI examined how changes in the forint’s exchange rate have passed through to domestic inflation since 2010. The model estimates suggest that in 2010 the exchange-rate effect was relatively modest: a 1% depreciation of the forint, with a lag of two quarters, raised the consumer price index by roughly 0.2 percentage points. By 2013 this effect had gradually weakened, to around 0.13 percentage points, before rising sharply thereafter. The inflationary impact of exchange-rate movements intensified, with the pass-through reaching about 0.5 by 2018, at a time when the exchange rate itself was showing greater volatility. As a result, the weakening forint contributed significantly to the emergence of a high-inflation environment up to 2022 (the pass-through peaked that year at 0.65 percentage points). One reason for the strengthening exchange-rate effect is that the weight of imported goods in the consumer basket increased, (partly as a consequence of rising prices).

According to GKI’s estimates, the forint’s appreciation in 2025 helped to moderate the consumer price index. The effect, however, is not immediate: it appears with a lag of two to three quarters and largely fades within roughly a year. One explanation lies in inventory dynamics. As stocks purchased at weaker exchange rates are gradually run down, cheaper imports begin to filter through into retail prices.

Impact of a 1% depreciation of the forint on

the increase in the consumer price index (%)*

Source: GKI model estimates (2026). *In the case of a forint appreciation, the figure shows the moderating effect on the price index; that is, a strengthening forint reduces inflation by the indicated magnitude.

The model makes it possible to decompose inflation into an exchange-rate effect and other, predominantly domestic, factors. It is important to stress that the annual results do not reflect solely the direct impact of exchange-rate movements in a given year. Rather, they also capture the longer-term, lingering effects of earlier currency shifts. Exchange-rate changes do not feed into prices immediately or in full. Instead, their impact unfolds over several quarters, gradually filtering through to the consumer price index.

Az adatok szerint az árfolyamhatás különösen 2020-ban és 2022-ben volt magas. 2020-ban a forint leértékelődése akadályozta meg a defláció kialakulását, míg 2022-ben az árfolyamgyengülés érdemben hozzájárult ahhoz, hogy a fogyasztói árindex közel 15 százalékra ugrott. Becsléseink alapján a forint gyengülése nélkül ebben az évben (minden egyéb tényező változatlansága mellett) az infláció nagyjából 8 százalék körül alakult volna.

According to the data, the exchange-rate effect was particularly pronounced in 2020 and 2022. In 2020, the forint’s depreciation helped prevent the onset of deflation, while in 2022 the currency’s weakening contributed substantially to the consumer price index jumping to nearly 15%. Our estimates suggest that, without the forint’s depreciation (all other factors held constant), inflation that year would have been around 8%.

Decomposition of the consumer price index into

exchange-rate effects and other factors, 2011–2025 (%)

Source: GKI calculations (2026), based on data from KSH and Investing.com.

In contrast, in 2023 the forint’s appreciation helped moderate high domestic inflation, reducing the rate of price increases by roughly two percentage points, though inflation remained well above the previous year’s level. This reflects, in part, that the disinflationary effect of the 2023 appreciation offset the lingering inflationary impact of the significant depreciation in 2022, so that overall the exchange-rate effect acted to lower inflation.

In 2024, of the 3.7% rise in the consumer price index, 1.6 percentage points were attributable to the forint’s depreciation. This underscores how, in an open economy like Hungary’s, exchange-rate movements have a significant impact on the domestic price level.

In the fight against inflation, the Hungarian National Bank has sought, among others, to curb price pressures by keeping the base interest rate high. Higher rates both restrain domestic credit demand (and, by extension, consumption) and make forint-denominated assets more attractive to foreign investors. This boosts demand for the forint—through inflows of “hot money”—leading to currency appreciation and, in turn, reducing imported inflation. The forint strengthened significantly in the third and fourth quarters, which is expected to lower the 2026 price level by 2.3 percentage points in the first half of the year. The effect is already visible in the relatively favourable 2.1% inflation reported for January 2026.