In the article series of GKI Economic Research Co., we present the short- and long-term economic challenges facing the new Hungarian government. In the second part of our series, we deal with the productivity in Hungary.

In recent years’ economic policy debates, a recurring question is whether the competitiveness of the Hungarian economy has improved significantly, and whether this has actually brought the country closer to the more developed economies of the EU, or whether the gap has persisted. Hungary’s economic performance has improved significantly in several sectors over the past 15 years. However, this development—where it was faster than the EU average—has not proven sufficient to achieve wide-ranging convergence with the EU.

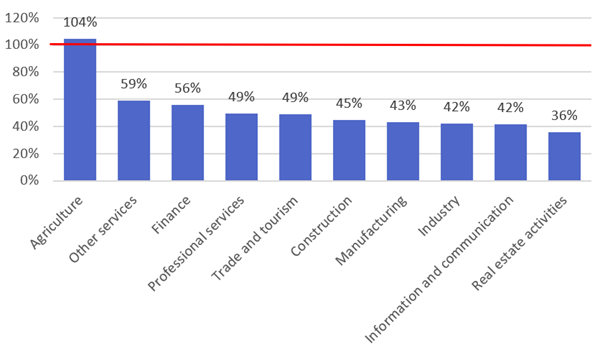

Sectoral productivity in Hungary compared to the EU average, 2025 (%)

Source: Eurostat: gross value added, employment, GKI calculations

Based on the 2025 data, agriculture stands out, where domestic productivity slightly exceeds the EU average (104%). The reason for this is that many people work as entrepreneurs, so entrepreneurial incomes also increase productivity per capita. In addition, large-scale, less intensive production requires low labor input, while EU subsidies represent a proportionally larger share of revenues due to lower wages. “Other services” (e.g. repair, household and small personal services) perform at a medium level (60% of the EU average). The largest gap is observed in real estate activities (36% of the EU average). Manufacturing and the information and communication sector are also in a weak position (40–42% of the EU average), which is particularly important, as these are among the higher-weight sectors.

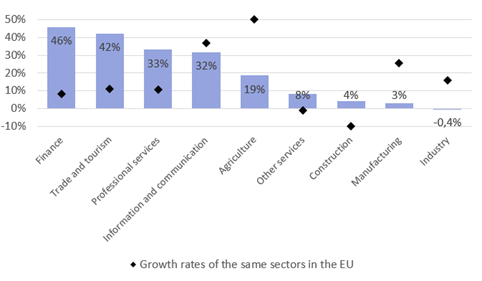

Between 2010 and 2025, significant progress was made in several sectors. The strongest improvement can be observed in the financial sector, where productivity increased by 46 percent (EU average +8%), followed by trade and tourism (+42%, compared to the EU’s +11%), professional services (+33%, EU average: +11%), and information and communication (+32%, EU average: +37%).Some parts of the service sector were able to grow faster because they adapted more flexibly to changes (e.g. internet-based solutions and, more recently, the use of AI), thereby increasing value added even with a declining workforce. Agriculture also saw improvement (+19%, EU average: +50%), although at a much more moderate pace. In contrast, there was virtually no significant change in industry and other capital-intensive sectors (-0.4%, EU average: +16%), while construction shows only modest growth (+4%, EU average: -10%).

Productivity growth by sector in Hungary and the EU (%), 2010–2025

Source: Eurostat

The figures also show that higher growth is not, in itself, a guarantee of a better position. Hungary has recorded rapid development in several sectors, yet it has only been able to move closer to the EU average. One reason for this is the low base level. This means that convergence requires a persistently higher rate of productivity growth. It is also evident that sectors receiving significant state support have experienced the weakest productivity growth, which indicates strong market distortions (industry, construction). While the automotive and battery industries have received nearly one thousand billion forints in state support since 2020, industrial productivity has declined over the past 15 years.

In Hungary, a targeted sectoral policy would be justified: intervention is warranted where a sector has a realistic chance of convergence, but the market alone does not resolve investment, technological, or labor market barriers. Such areas may include the targeted, controlled, and performance-monitored support of knowledge-intensive services, industrial modernization, or export-oriented domestic manufacturing sectors.

Overall, Hungary has achieved substantial progress in several areas of productivity since 2010; however, it has by no means managed to catch up with the EU average. Certain sectors of the domestic economy have been able to grow faster than the EU average, but significant gaps remain. The most important question for the coming period is therefore whether this development can be sustained in the long term and whether it can bring Hungary closer to EU levels.