As a consequence of the 2008 Great Financial Crisis, the EU adopted new legislation starting in 2009 to strengthen credit ratings and enhance the protection of consumers and investors. These regulations mandate the transparent publication of methodologies used by credit rating agencies, whether for corporate or sovereign ratings. Furthermore, these institutions are obligated to review their methodologies continuously, at least on an annual basis. Should significant methodological changes occur that could impact ratings, they must be published one month in advance to provide stakeholders the informations.

Fortunately, the transparency resulting from these strict rules makes it easier to forecast the impact of euro adoption—or the first step toward it, joining the ERM II (Exchange Rate Mechanism)—on a member state’s credit rating. In this analysis, we examine how the new government’s euro adoption plans are expected to influence Hungary’s credit rating outlook and whether the resulting impact can offset the rising fiscal risks already highlighted by several rating agencies.

A country must spend at least two years in the ERM II system before adopting the euro to demonstrate the exchange rate stability of its national currency. Within this framework, the exchange rate may only deviate from a centrally defined central parity by +/- 15%. This entry rate is of paramount importance, as it serves as a guideline for the final EUR/HUF conversion rate at the time of adoption. Typically, the most recently joined member states introduced the euro at the ERM II entry rate or at a stronger level. In this regard, the case of Slovakia is particularly relevant; during its ERM II period, the currency was revalued twice. As a result, the Slovak koruna was ultimately pegged to the euro at a rate of 30.126, approximately 22 percent stronger than the initial entry level of 38.455.

Joining the ERM II mechanism is of key significance from the perspective of CRAs. Membership reflects macroeconomic stability and validates the intent for Eurozone integration to the markets, which can bolster investor and rating agency confidence.

Beyond general sentiment, accession can generate a direct positive impact within credit rating assessment models. This aspect is particularly prominent at Standard & Poor’s (S&P), where “monetary policy effectiveness” and the “exchange rate regime” constitute an independent assessment dimension. This category carries a weight similar to other major macroeconomic indicators in determining the final rating. S&P’s evaluation is critical because, among the “Big Three” agencies, Hungary’s rating currently stands at its lowest with them; the Hungarian sovereign debt is currently only one notch above the non-investment grade category. Furthermore, the outlook has been negative for over a year, which, based on S&P’s methodology, suggests a downgrade within a 0.5–2 year window. Most recently, the negative outlook signaled in the summer of 2022 was indeed followed by a downgrade in January 2023.

For Moody’s, ERM II entry could be equally significant. On one hand, it could lead to a strengthening in the assessment of monetary and macroeconomic policy effectiveness, which represents a 30 percent weight within the Institutions and Governance Strength pillar (one of the four main dimensions). On the other hand, regarding the Fiscal Strength pillar, it could override the outlook for the foreign currency debt trajectory. With euro adoption, the euro-denominated debt—which accounts for more than half of the total foreign currency debt—would effectively become local currency debt. Furthermore, in assessing Susceptibility to Event Risk, the commitment to a new exchange rate system maintained jointly with the ECB, and the subsequent euro adoption, reduces political, liquidity, and external vulnerability risks.

In Fitch’s methodology, within the External Finances pillar (accounting for 17.3 percent of the final rating), Eurozone members uniformly receive a positive score for reserve currency flexibility. This reflects a low probability of financing difficulties due to stable demand for issued assets. However, during the ERM II entry phase and while operating the fixed exchange rate system, the agency treats this as a primary risk. It scrutinizes foreign exchange reserves and financial sector stability more strictly, as a potential exchange rate failure within a fixed regime could be detrimental to sovereign creditworthiness. For Fitch, euro adoption would also bring a clear improvement in the fiscal dimension regarding the share of foreign currency debt.

According to research by the European Commission, the methodologies of CRAs allow for credit rating improvements from the moment of ERM II admission until actual euro accession. This implies that joining ERM II does not automatically result in an immediate upgrade; rather, it requires proof of stable participation within the system. The analysis suggests that rating agencies particularly value the “reserve currency” status of the euro.

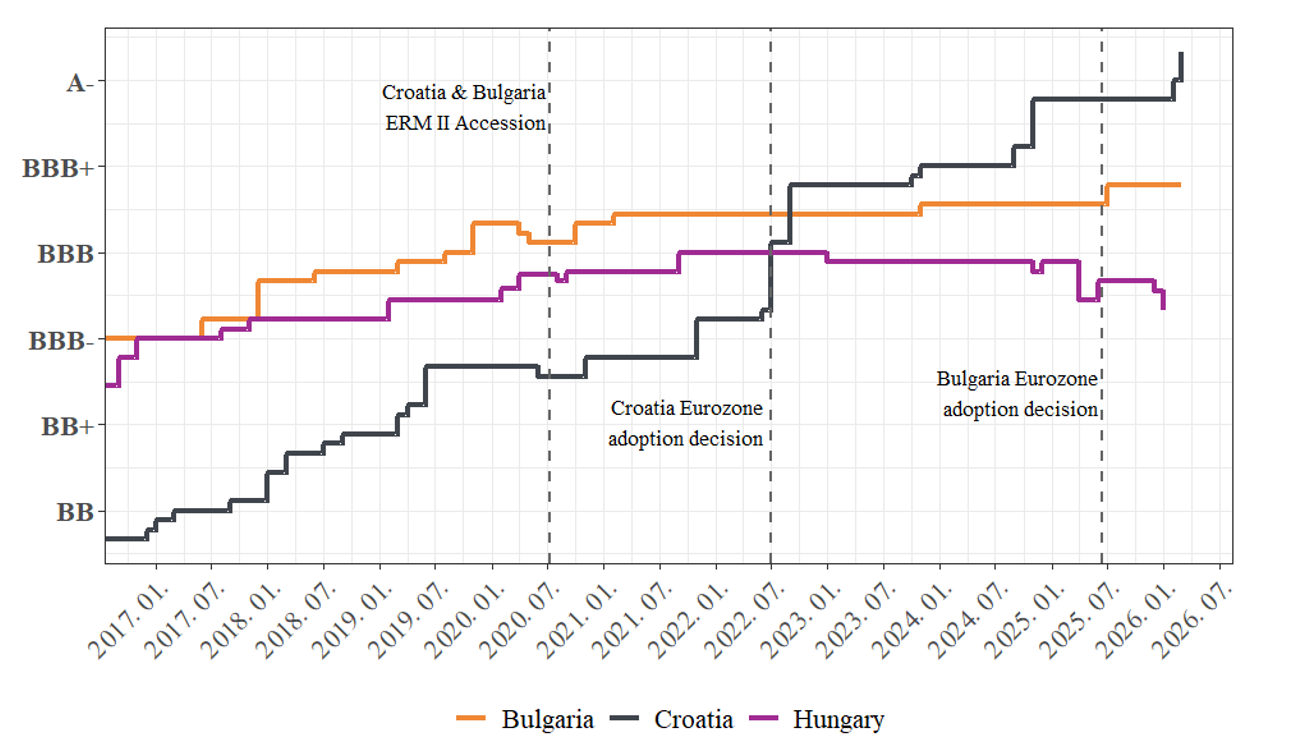

ERM II accession did not result in an immediate rating upgrade for Croatia or Bulgaria either; instead, the rating outlooks became more positive. In Croatia’s case, the assessment of ratings improved gradually, and then, in connection with the announcement of the euro’s introduction, the perception of Croatian sovereign debt improved significantly.

Sovereign Credit Ratings of Hungary, Croatia, and Bulgaria[1] (2017–2026)

Source: GKI calculations, The Global Economy

Overall, credit rating agencies may view ERM II entry as a vital milestone on the road to euro adoption. Since all three major institutions strive to “smooth” their ratings, this expected positive shift could offset the currently explicitly signaled fiscal risks. Consequently, progress regarding ERM II accession in the coming months could be crucial in ensuring that, despite maintaining negative outlooks, these institutions allow time for the strengthening of fiscal prospects during their spring and autumn reviews.

[1] The average credit rating of S&P, Fitch, and Moody’s, taking into account the assigned outlook.