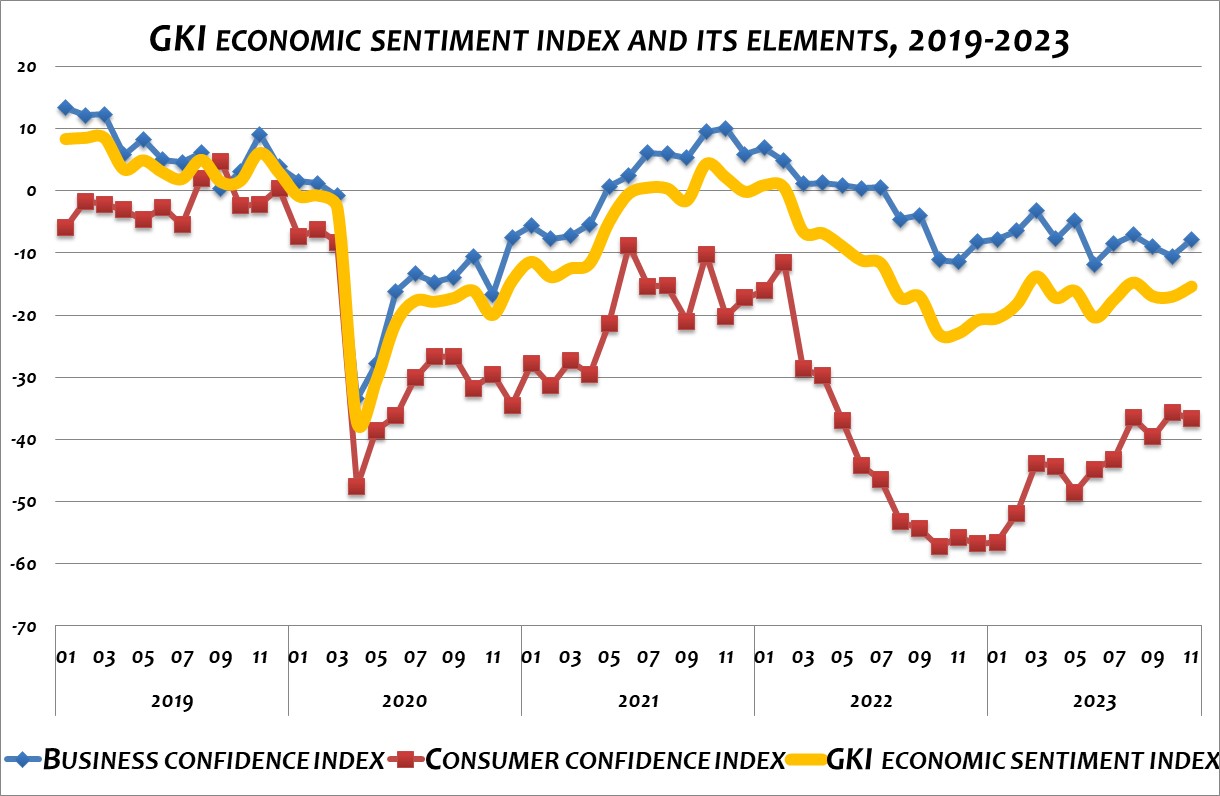

Consumers are slightly more pessimistic about the near future in November, while the business world is somewhat more optimistic than in October, according to a survey conducted by GKI Economic Research Co. with EU support. The GKI economic sentiment index rose markedly, firms’ employment expectations improved and their plans to raise prices declined compared to the previous month.

The GKI Business Confidence Index rose markedly (by 3 points) in November, after declining in September and October. In the last month of autumn, the outlooks for industry and in particular business services improved, while for the construction sector was little changed and for retail trade was slightly less positive. In industry, the assessment of total inventories remained within the statistical margin of error, while the value of own-account inventories and the production outlook for the next 3 months improved significantly compared to October. In construction, the assessment of order books deteriorated but the employment outlook improved. In the retail trade sector, satisfaction with business performance in the previous 3 months deteriorated markedly and the level of inventories rose slightly, while the assessment of orders expected in the next 3 months remained unchanged. In the services sector, although business sentiment deteriorated slightly in the previous three months, turnover and employment expectations for the next three months were also markedly better than in October.

The GKI consumer confidence index has been on an upward trend this year, setting a one-and-a-half-year record in October. However, November brought a slight negative correction, with the index falling within the statistical margin of error compared to October. The public perceived their own financial situation over the past 12 months to have deteriorated slightly compared to the previous month. At the same time, the financial outlook for the next 12 months and the perception of own money to spend on high-value purchases remained little changed.

Businesses’ willingness to employ improved slightly in November compared with the previous month, with the proportion planning to lay off and increase their workforce almost equal. Pessimists are in the majority in the construction sector, while optimists dominated the services sector. In industry and retail trade, the two proportions are essentially equal. The public’s fear of unemployment has risen somewhat compared to October.

The overall price increase plans in the business sector fell markedly in the eleventh month of the year and consumers’ inflation expectations also eased compared with October. Businesses and households have different views of the future outlooks for the Hungarian economy: while the former’s view has improved slightly, the latter’s has deteriorated slightly after several months of improvement.

Explanation to the methodology:

In line with the methodology used by the European Commission, GKI surveys the expectations of industry, trade, construction, services (the latter, as in the EU, excludes financial and public services) and households in the calculation of its business confidence index. GKI’s economic sentiment index is the weighted average of the consumer confidence index and the business confidence index.

The business confidence index is the weighted average of the industrial, trade, construction and services confidence indices. The industrial confidence index is derived from the responses to questions on business perceptions of incoming orders and inventories, and on production expectations. The construction confidence index is the average of the perception of incoming orders and employment expectations. The trade confidence index is the average of business and inventory level perceptions and turnover expectations. The services confidence index is the average of business activity assessment, expectations for turnover and employment. GKI publishes seasonally adjusted data by using appropriate mathematical method (the Tramo Seats method) to filter out the discrepancies caused by seasonal effects (e.g., differences in weather conditions between winter and summer, increased demand before Christmas, lower output because of summer vacations).

The consumer confidence index is compiled from responses to questions concerning the past and expected financial position of households, the expected economic situation of the country, and the prospects for purchasing consumer durables.